A year ago, we examined Laurus Labs as a company in transition, moving beyond its traditional antiretroviral (ARV) business toward becoming a diversified pharmaceutical powerhouse.

Visit our earlier analysis: A closer look at Laurus Labs beyond the market noise

Today, from a fundamental analysis standpoint, we revisit that journey to see how the strategy has evolved into tangible execution.

Laurus Labs operates across three key business segments: Active Pharmaceutical Ingredients (APIs), Finished Dosage Forms (FDF), and Contract Development and Manufacturing (CDMO), each contributing differently to overall financial performance. With manufacturing facilities approved by USFDA, EMA, WHO, and PMDA, the company serves major regulated markets globally.

The Big Shift: CDMO Takes Centre Stage

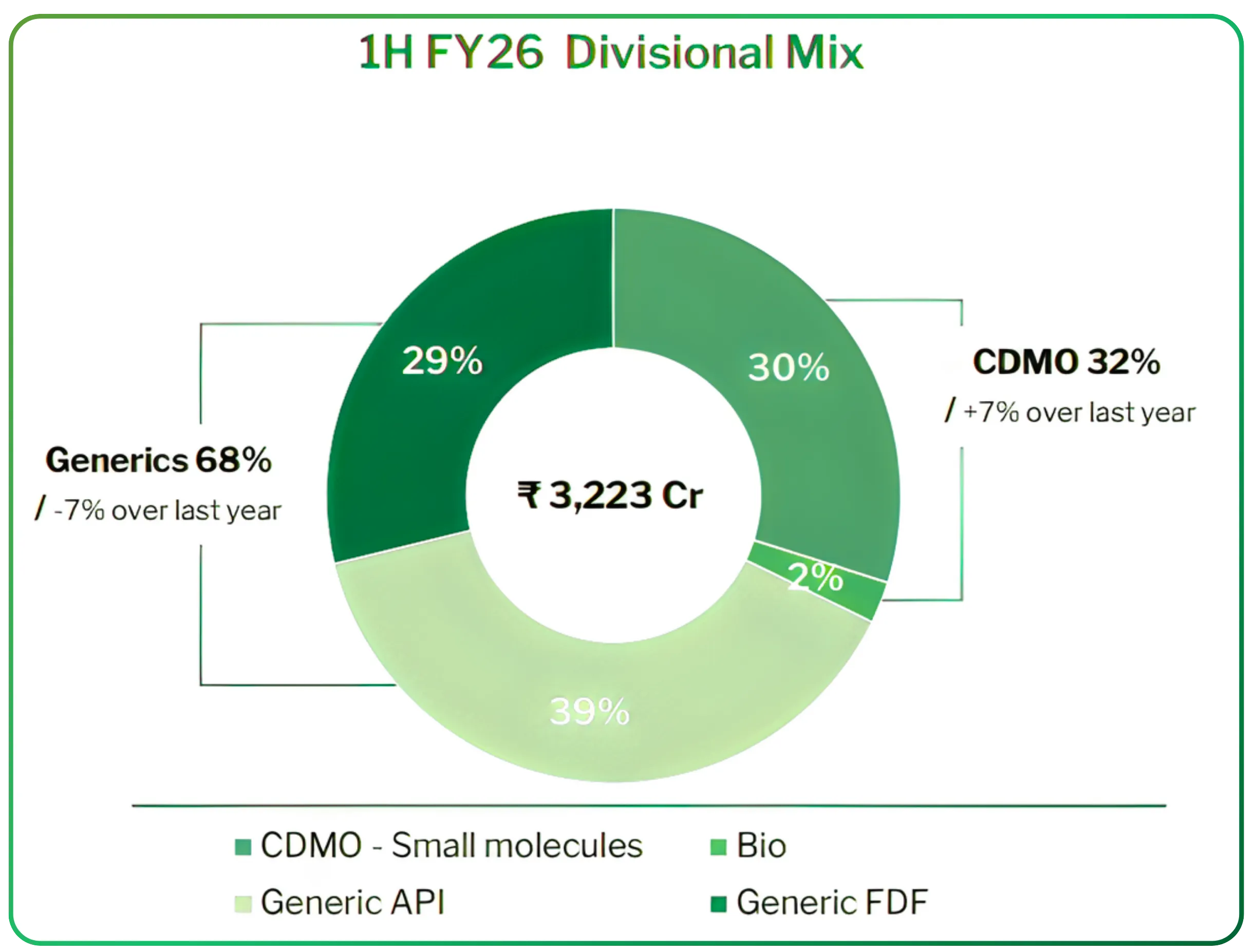

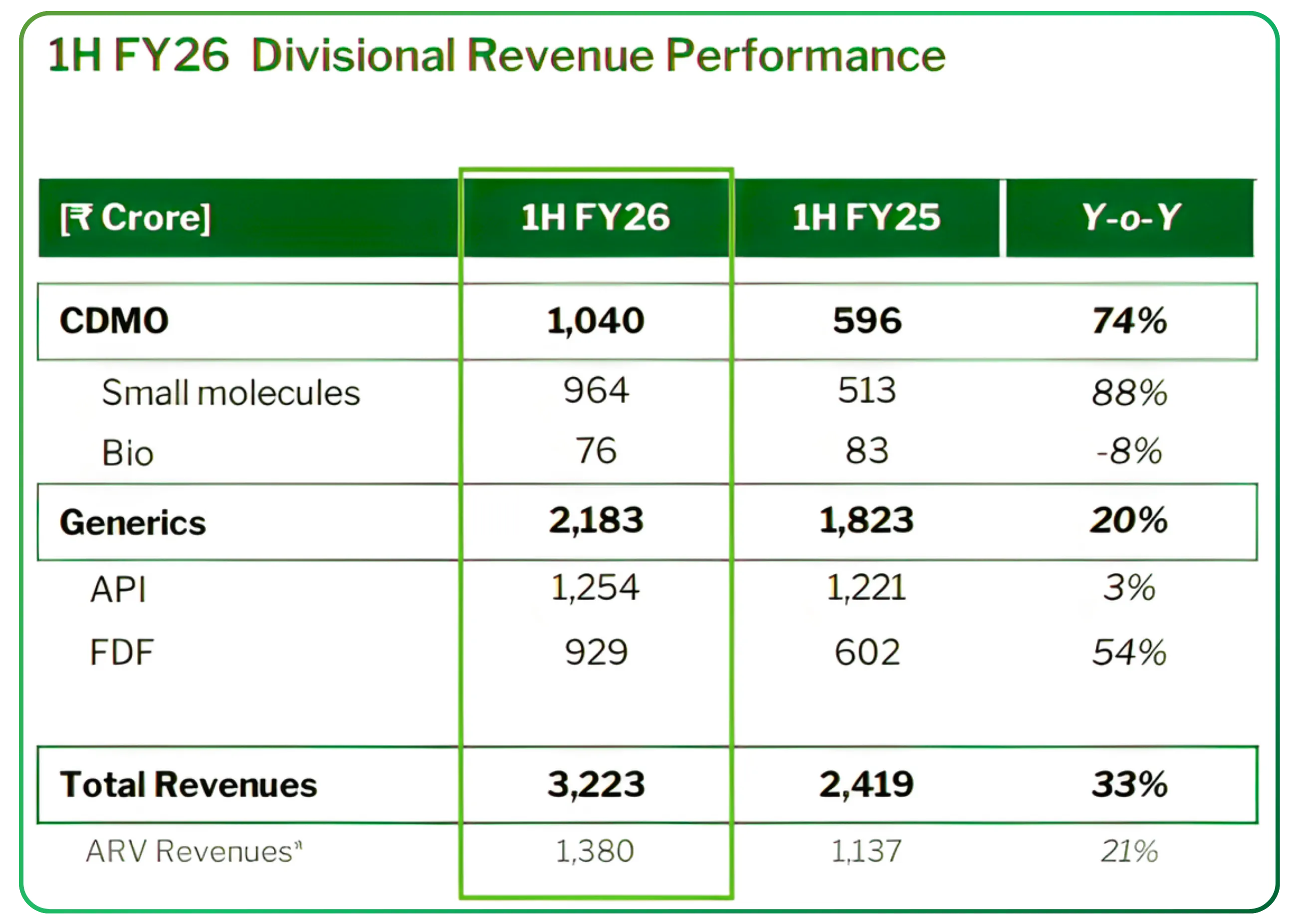

The most significant development over the past year has been the rapid scaling of Laurus' CDMO business. Just three years ago, CDMO contributed only 15-16% of revenues. By the first half of FY26, this figure jumped to 30-32%—a doubling in just three years.

CDMO has moved from a secondary segment to a core growth driver, with management targeting a 50% revenue contribution over the medium term.

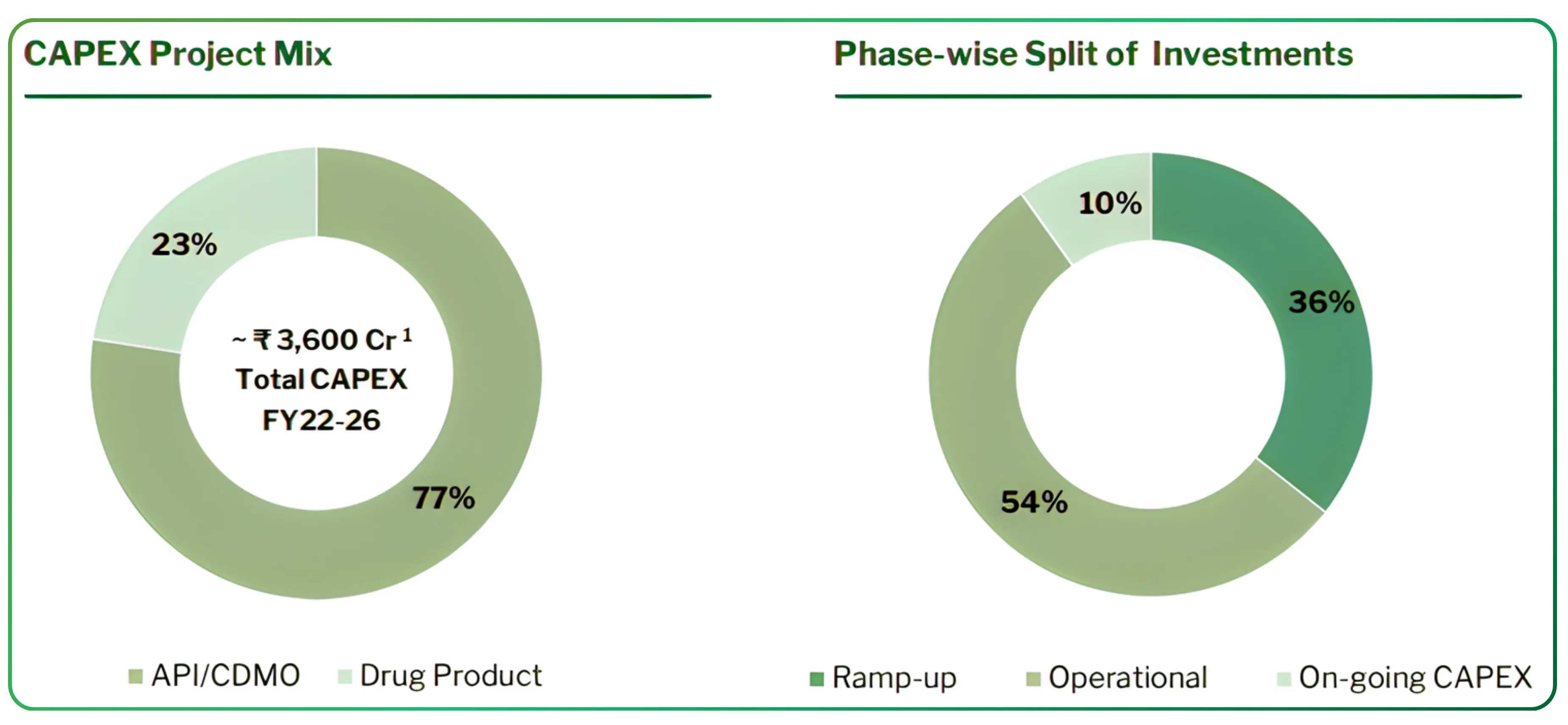

This transformation didn't happen overnight. Between FY22 and FY26, Laurus invested approximately ₹3,200 crore in expanding its capabilities, with 77% directed toward API and CDMO infrastructure. The company is now targeting CDMO to contribute 50% of total revenues in the coming years.

This shift has materially altered the revenue growth profile of the company and has become a key driver influencing sentiment around laurus labs shares.

Building for Scale: The ₹4,500 Crore Question

In Q2 FY26, Laurus announced its most ambitious expansion yet—a $600 million (approximately ₹5,000 crore) investment over eight years. The Andhra Pradesh government allocated 532 acres for developing a large pharmaceutical manufacturing complex focused on CDMO, APIs, drug products, and biotechnology.

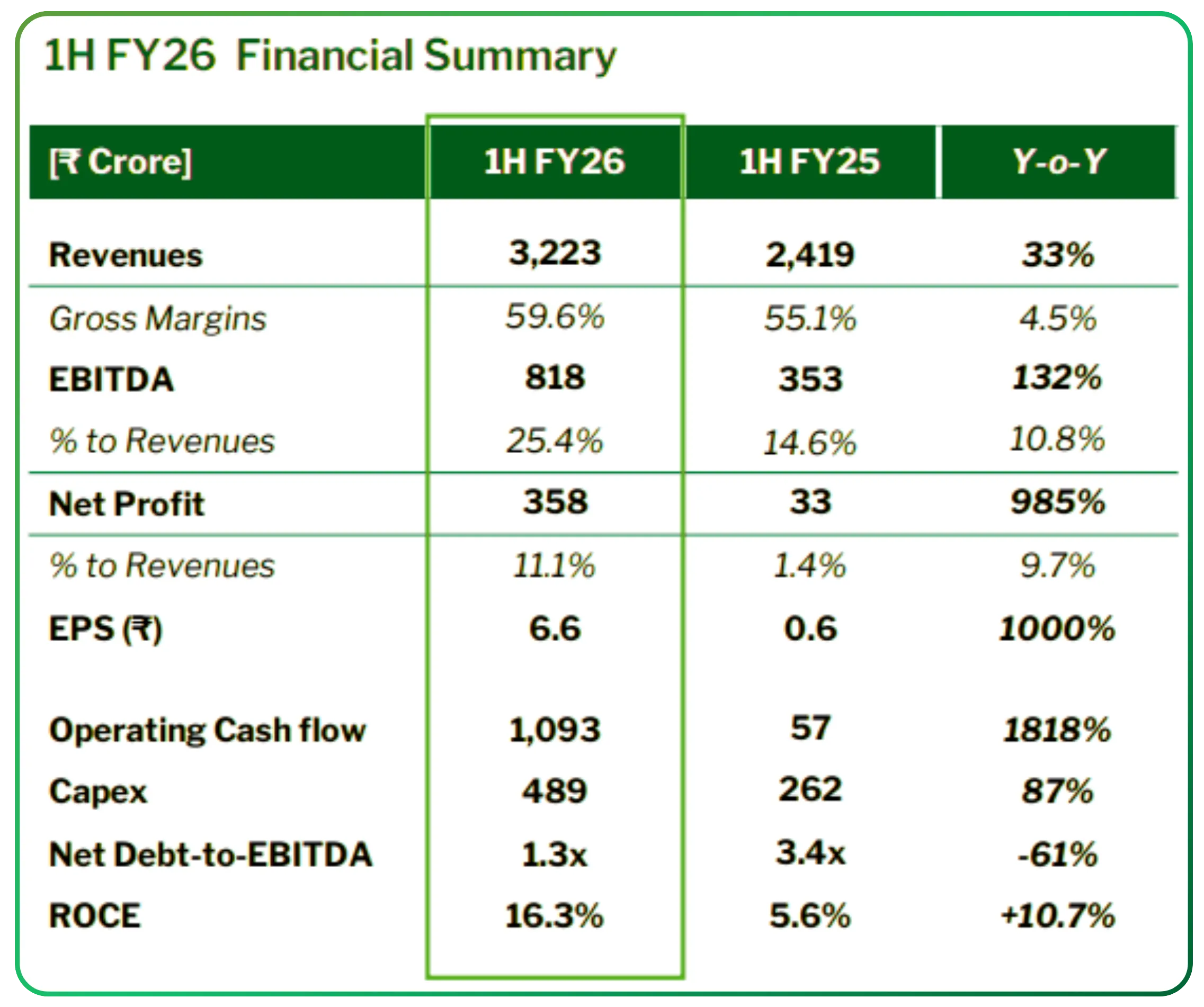

Unlike the heavy capex cycle of FY22-FY25 that pressured margins, this investment comes at a different stage.The company generated ₹1,000 crore in operating cash flow in H1 FY26 alone, supporting expansion while keeping the capital structure under control.

Strength: From Projects to Revenue

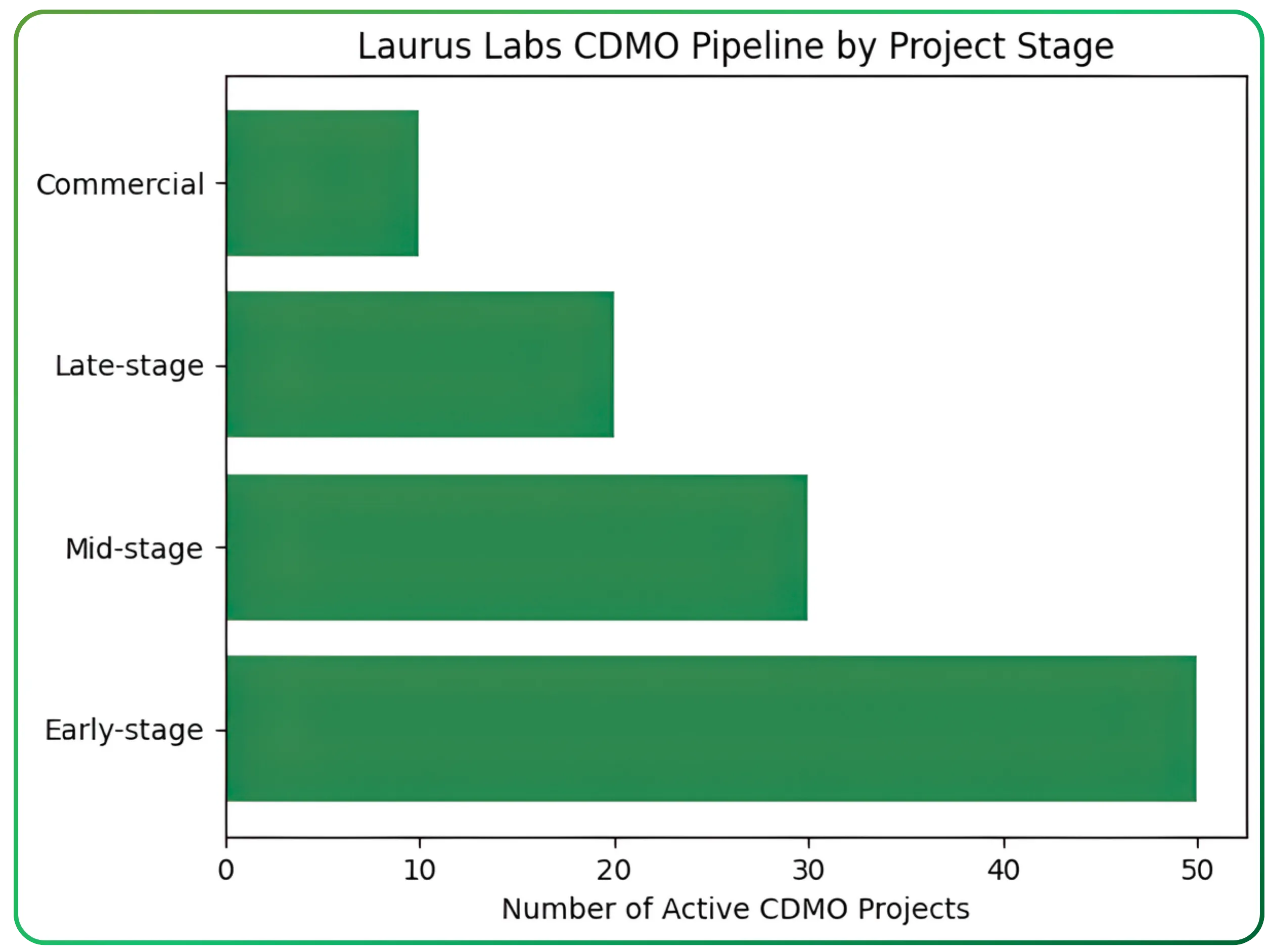

As of Q2 FY26, Laurus has built 110 active projects on CDMO. These span complex small molecules, biocatalysis, flow chemistry, and fermentation—with an increasing proportion in mid-to-late stage and commercial programs.

The company has filed approximately 90 Drug Master Files (DMFs), providing regulatory pathways for future commercialization.

For a different example of an asset-driven business model, you may also read Seamec Ltd Operating an Asset-Driven Offshore Services Business, a focused analysis from the offshore services sector.

Laurus’ CDMO pipeline shows strong depth at the early and mid stages, with a growing base of late-stage and commercial programs that underpin future revenue conversion.

Of the 110+ CDMO projects, a majority are linked to human health applications, with increasing exposure to oncology drugs, alongside early-stage programs in animal health and crop science.

Strategic Partnerships: Laying Foundations for Tomorrow

KRKA Joint Venture

Laurus announced a joint venture with KRKA, a Slovenia-based generic pharmaceutical major. KRKA holds 51% and Laurus 49% in this partnership.The ground-breaking ceremony for the Hyderabad formulations facility took place in June 2025, with Phase-1 commissioning targeted for mid-2027.

ImmunoACT: Cell Therapy Goes Mainstream

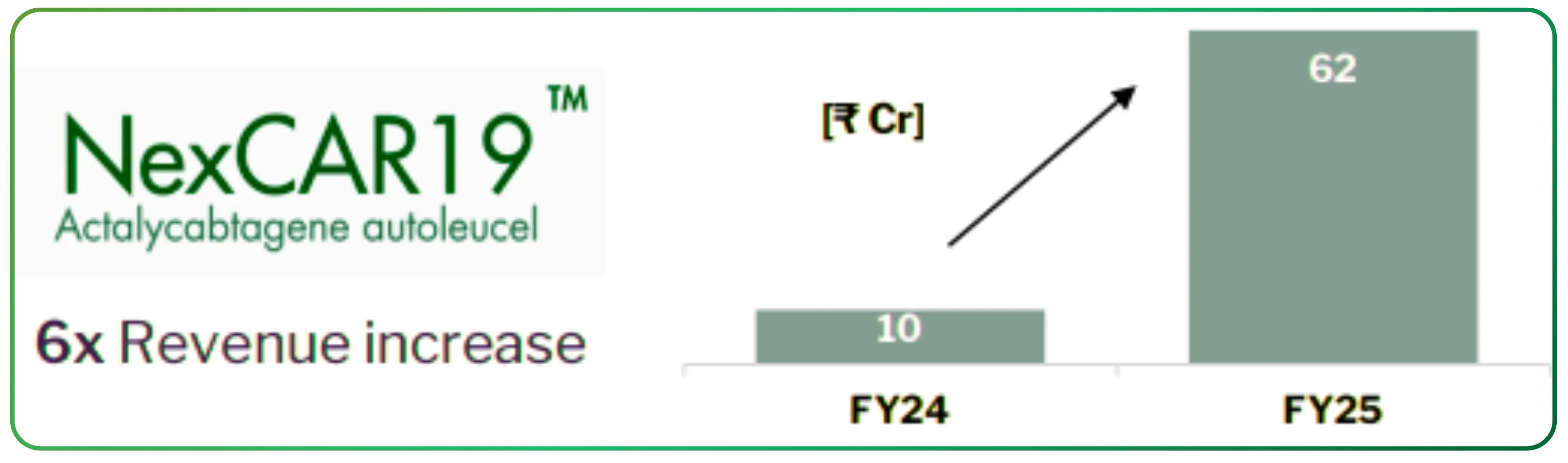

Laurus' strategic investment in ImmunoACT (holding approximately 34% stake) has begun showing results. ImmunoACT specializes in CAR-T cell therapy—a breakthrough cancer treatment that reprograms a patient's immune cells to fight cancer.

The revenue jumped 6x year-over-year, from ₹10 crore in FY24 to ₹62 crore in FY25. The company has already treated around 350 patients, with treatment costs at roughly one-tenth of what patients pay in developed markets. The new Navi Mumbai facility aims to scale capacity to approximately 2,500 treatments per year by FY26.

V. Simpson Emmanuel (former Managing Director and CEO of Roche Pharma India with nearly three decades of pharmaceutical experience) recently joined ImmunoACT as President.

New Revenue Avenues

Laurus' 2020 acquisition of Richcore Lifesciences (now Laurus Bio) marked its entry into biotechnology and biologics. This move positions the company beyond traditional small-molecule chemistry into precision fermentation and bio-manufacturing.

The strategic logic is clear: fermentation offers fewer process steps, higher selectivity, better scalability, and improved sustainability compared to traditional chemistry—making it ideal for next-generation complex molecules.Tripling fermentation capacity from 200,000 liters to 600,000 liters by end of FY27,

OLED Materials: In October 2025, Laurus announced an MoU with LORDIN Co., Ltd (South Korea) to collaborate on OLED materials development and supply—Laurus' entry into the advanced materials space in India.In December 2025, LORDIN announced a major breakthrough in high-efficiency blue phosphorescent OLED emitters, confirming commercial feasibility after six years of R&D. The partnership aims to combine Laurus' chemical synthesis expertise with LORDIN's proprietary OLED technology.

This is clearly a long-term opportunity unlikely to impact revenues in the near term, but represents interesting diversification optionality for the future.

The Customer Profiles

- Amgen: One of the top 15 global pharma/biotech firms. Shipment quantities have grown from zero in mid-2024 to regular monthly shipments by late 2025.

- Catalent: A global CDMO leader. When tier-1 CDMOs source from other CDMOs, it validates real capability gaps being filled.

- AMPAC Fine Chemicals: A high-end US innovator-focused CDMO specializing in potent, complex molecules.

- Ajinomoto: The global leader in industrial fermentation and amino-acid production. While still in the testing/trial phase, engagement with such a demanding customer validates Laurus' fermentation capabilities.

Industry sources also suggest deepening engagement with other global innovators including Pfizer, Vertex, PTC, Merck, and potential conversations with Eli Lilly and Novo Nordisk.

For a different example of strategic capital allocation in a holding company, you may also read Zuari Industries Limited Viewed Through Assets and Capital Returns

Advanced Chemistry Capabilities: Building Competitive Moats

Laurus has invested in several next-generation platforms that distinguish it from traditional Indian CDMOs:

Flow Chemistry: While most Indian CDMOs focus on batch chemistry, flow chemistry remains limited to a handful of players. In contrast, multiple Chinese CDMOs have scaled flow chemistry capabilities. If the BioSecure Act drives US innovators to diversify away from China, they'll expect comparable capabilities from Indian partners—positioning Laurus advantageously.

Biocatalysis and Fermentation: Leveraging biological catalysts and organisms for cleaner, more efficient chemical processes.

Peptides and ADCs (Antibody-Drug Conjugates): Complex oncology therapeutics representing the cutting edge of targeted cancer therapy.

Cell & Gene Therapy: Through ImmunoACT partnership, gaining exposure to one of the fastest-growing segments in biopharma.

Financial Recovery: The Turnaround is Real

After a challenging FY23-FY25 period marked by high capex and asset under-utilization, the financial picture has improved materially:

- Net debt-to-EBITDA has reduced significantly as cash flows improved

- Operating cash flow reached ₹1,000 crore in H1 FY26 alone

- Margins are recovering as asset utilization improves

- ARV business has stabilized at around ₹2,500 crore annual revenue (±₹200 crore)

Management commentary from the December 2025 ET NOW interview highlighted "very good visibility of revenue for the next 6 to 12 months," suggesting confidence in execution.

Compared with past performance, the recovery in operating profit and net income signals that the earnings rebound is supported by cash flows rather than accounting reversals.

Why This Time Feels Different

The key difference between the current capex cycle and the painful FY22-FY25 period is the strength of the underlying business:

- Product mix is richer: Higher CDMO contribution with better margins

- Scale is larger: Revenue base has grown substantially

- Cash generation is stronger: ₹1,000 crore OCF in just six months

- Capex is phased: $600 million spread over eight years, largely internally funded

- Financial discipline: Management committed to keeping net debt below ~50% of revenues.

Key Developments in the Last 12 Months: A Summary

| Development | Timeline | Significance |

|---|---|---|

| CDMO revenue reaches 30–32% | H1 FY26 | Doubled from ~15% three years ago |

| ₹5,000 crore capex announcement | Q2 FY26 | 532 acres allocated for integrated pharma complex |

| KRKA JV groundbreaking | June 2025 | Phase-1 commissioning targeted for mid-2027 |

| ImmunoACT revenue 6× growth | FY25 | ₹10 cr → ₹62 cr; ~350 patients treated |

| V. Simpson Emmanuel joins ImmunoACT | 2025 | Former Roche India CEO appointed as President |

| LORDIN OLED partnership | Oct 2025 | Entry into advanced materials segment |

| LORDIN blue OLED breakthrough | Dec 2025 | Commercial feasibility successfully confirmed |

| Fermentation capacity tripling plan | Dec 2025 | Capacity expansion from 200,000L to 600,000L by FY27 |

| New tier-1 customers onboarded | 2025 | Amgen, Catalent, AMPAC, Ajinomoto added |

| Strong H1 cash generation | H1 FY26 | ₹1,000 crore operating cash flow |

The Risks Remain Real

No investment thesis is complete without acknowledging risks:

- Execution Risk: Scaling CDMO while deploying heavy capex simultaneously is challenging. Any faltering could impact sentiment quickly.

- Quality and Compliance: As Laurus onboards more demanding customers, quality issues could delay programs. However, the company's track record here has been strong.

- Regulatory Risk: USFDA observations remain a permanent overhang for any pharma manufacturer, though Laurus has navigated this well historically.

- Customer Concentration: While diversifying, losing a major CDMO program could impact growth trajectory.

- Geopolitical and Policy Risk: Benefits from BioSecure Act are potential upsides, not certainties.

Verdict: From Noise to Signal

A year ago, Laurus was a story of potential—a company attempting to transform from an ARV-focused player to a diversified pharmaceutical powerhouse. Today, that transformation is measurably underway.

The CDMO business has scaled from 15% to 30% of revenues. The pipeline has expanded to 110+ projects. New tier-1 customers are being onboarded. ImmunoACT is treating hundreds of cancer patients. Fermentation capacity is tripling. Strategic partnerships with KRKA and LORDIN are progressing.

Most importantly, the company is generating strong cash flows while maintaining financial discipline—suggesting this isn't just growth for growth's sake, but sustainable expansion backed by operational improvements.

The market has taken notice, but sentiment remains divided. For long-term investors, the question isn't whether Laurus is executing—the numbers clearly show it is. The question is whether this execution can sustain through the next phase of expansion.

What's clear is that Laurus isn't just expanding the present. It's systematically engineering the future—across CDMO, biologics, cell therapy, and advanced chemistry platforms. Whether this vision fully materializes will depend on execution over the coming years, but the foundation is unmistakably being laid.

From a valuation lens, the market is no longer pricing Laurus Labs purely on recovery. The debate now centres on fair value, how it compares with intrinsic estimates, and whether current prices justify fresh investment decisions after the sharp rerating.

Turn research into action — trade smarter on CubePlus.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.