Most investors view Vaibhav Global as a traditional television shopping company. At first glance, it appears to be a business facing the impact of viewers moving away from cable TV, a slowdown in Western consumer spending, and persistent currency headwinds.

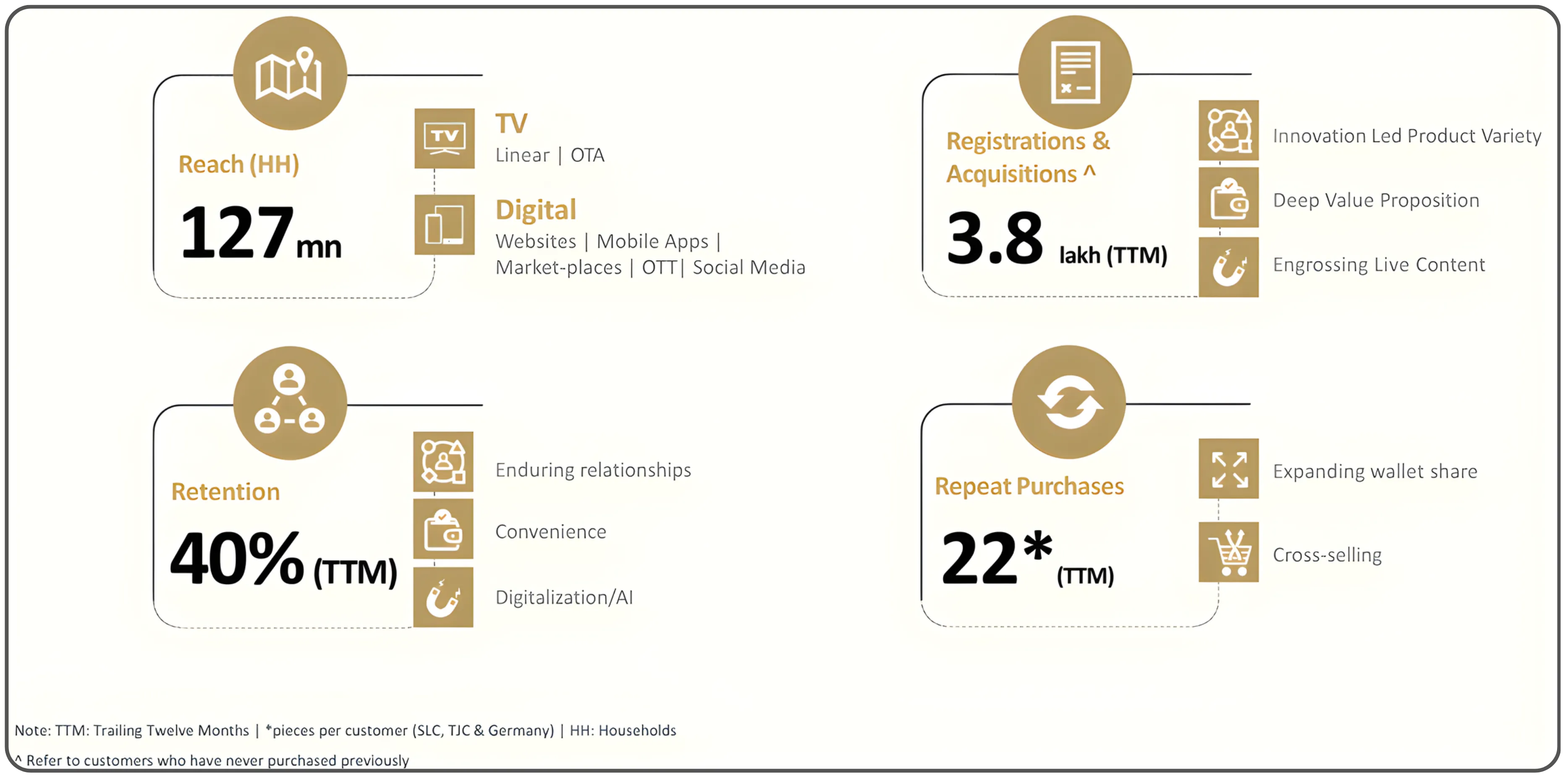

A closer examination, however, reveals a more nuanced narrative. Vaibhav Global is a vertically integrated, direct-to-consumer jewellery and lifestyle business that makes products in Jaipur and sells them to over 127 million households across the United States, United Kingdom, and Germany, without a single retail shelf, without a single distributor, and without spending a rupee on physical retail presence. Its gross margins have held above 60% through inflation, tariff shocks, and a post-COVID demand normalization. The balance sheet carries net cash of ₹213 crore.

The Business

Vaibhav Global runs three major TV shopping channels:

- Shop LC in the United States

- TJC and Ideal World in the United Kingdom

- Shop LC in Germany

Each channel has its own website ( shoplc.com, tjc.co.uk, idealworld.tv, shoplc.de) where customers can shop online. And here's the important part: 42% of their sales now come from digital platforms, websites, mobile apps, and streaming services.

They've successfully transitioned from "TV-only" to "TV + Digital."

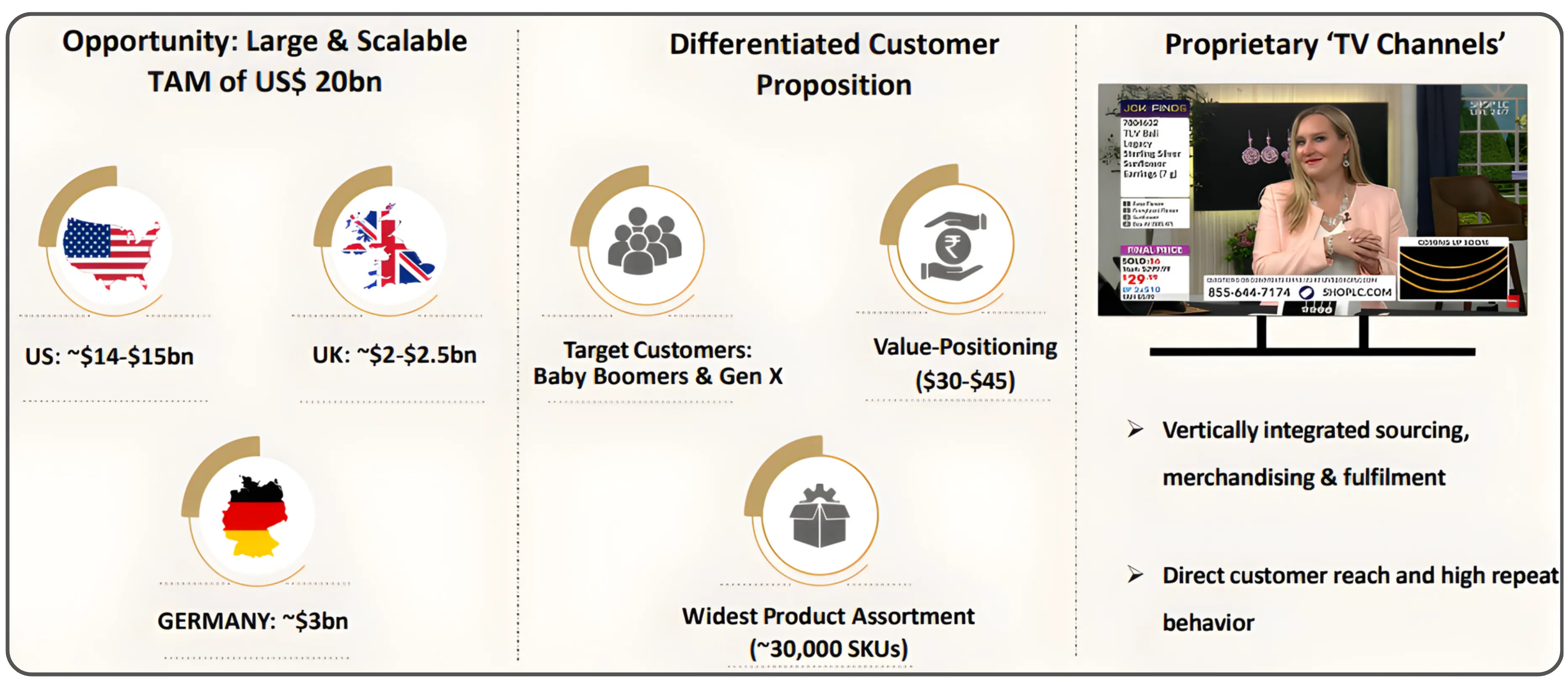

VGL manages around 30,000 different products at any time:

- 25,000 items in fashion jewellery, gemstones, and accessories

- 5,000 lifestyle products (home goods, electronics, beauty items)

VGL launches 100 new products every single day. That's 14,000 to 15,000 new jewellery designs each year.

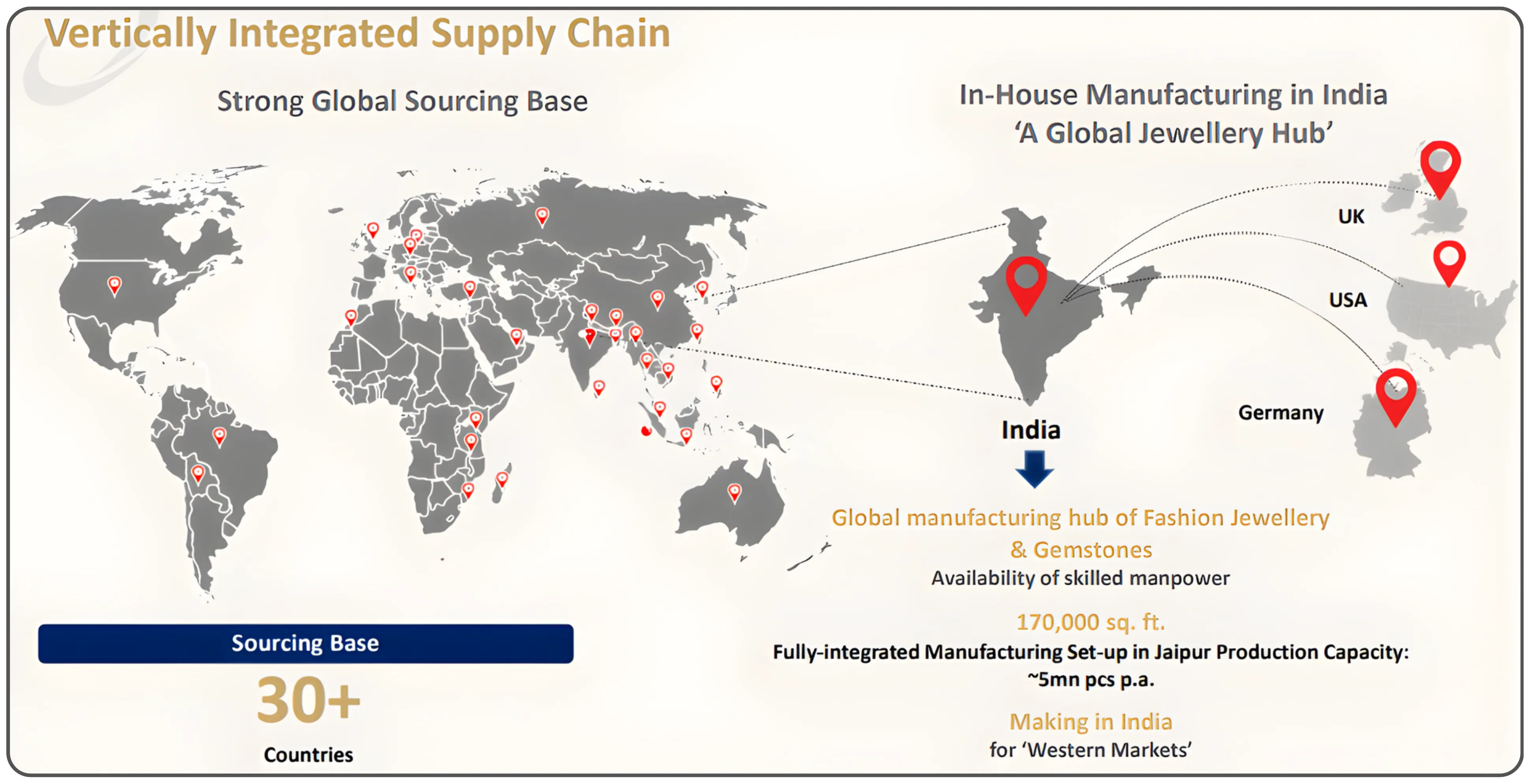

Production

VGL sources raw materials and gemstones from 30+ countries, manufactures through its 170,000 sq. ft. Jaipur facility (which handles 90% of its fashion and gemstone manufacturing at a capacity of 5 million pieces per year), and sells directly to the consumer through its own channels. This is what allows it to price affordably for the mass market while retaining industry-leading gross margins.

The Geography

Understanding VGL requires understanding where it operates, because the three geographies are at very different stages.

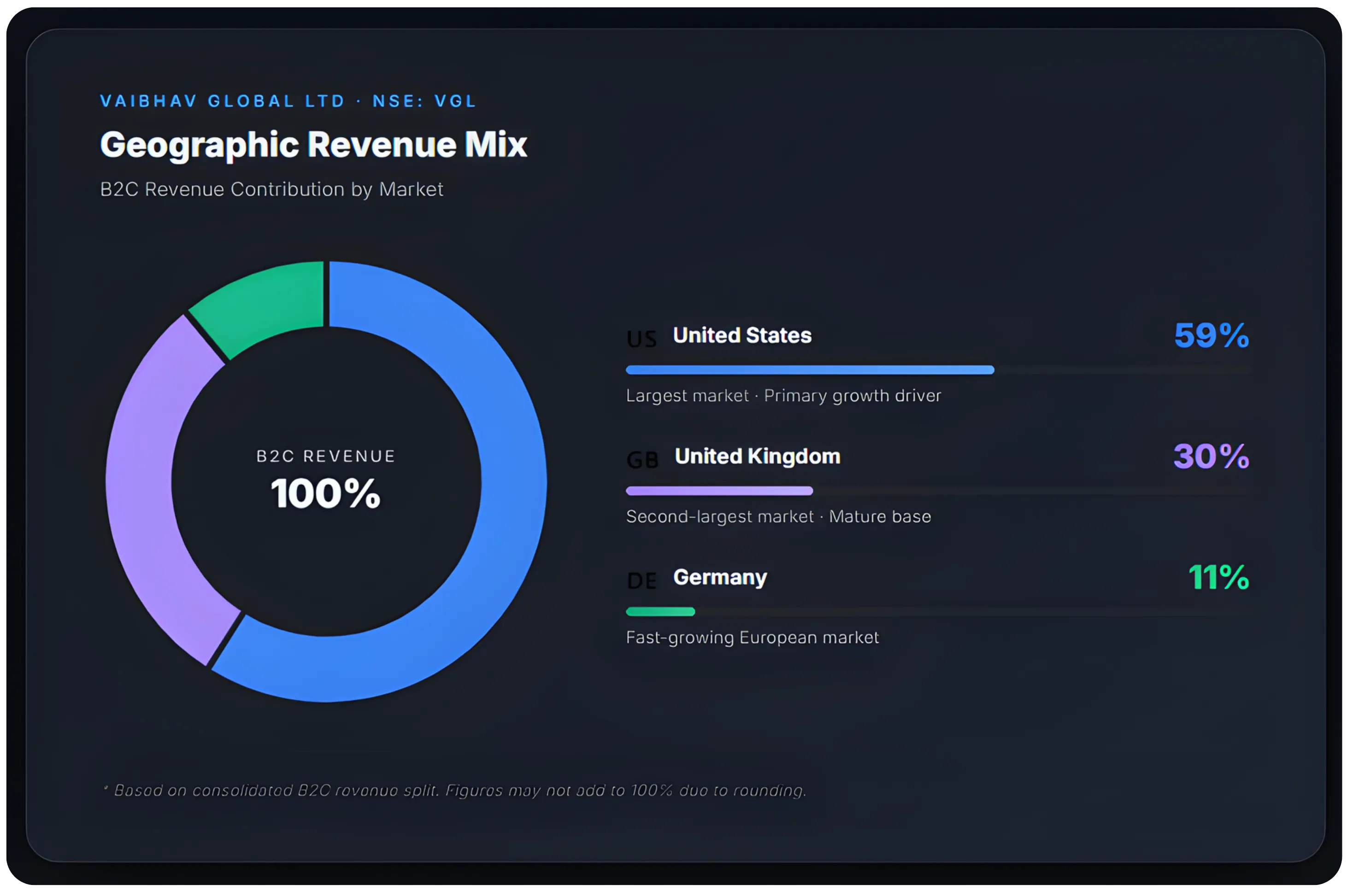

The United States is the largest market, contributing roughly 59% of consolidated B2C revenue. Shop LC reaches American homes through cable, satellite, and OTA broadcasts, and sells primarily in the $25–$50 price range, targeting Baby Boomers and Gen X buyers who value value-for-money fashion jewellery.

In Q3 FY26, the US delivered ₹593 crore in revenue, growing 3% in local currency. The United Kingdom contributed approximately 29% of revenue. VGL operates TJC (The Jewellery Channel) and has also integrated Ideal World, a general merchandise TV shopping channel acquired for just ₹12 crore in September 2023. In Q3 FY26, the combined UK business delivered ₹301 crore in revenue, and, more significantly, UK EBITDA grew 40% year-on-year. Ideal World, once considered a fixer-upper acquisition, has now reached EBITDA margins comparable to TJC. This is an underappreciated value unlock buried inside the segment numbers.

Launched initially as a small-scale experiment, Germany now contributes approximately 11% of group revenue. In Q3 FY26, it delivered €7.9 million in revenue (growing 5.1% in local currency) and, for the first time, reported segment-level EBITDA profitability of approximately 6%. Management attributed this to a 300–400 basis point improvement in gross margins through better product offerings, combined with cost rationalization across airtime costs, shipping partners, and warehouse productivity. The full-year FY27 target is consistent positive EBITDA contribution from Germany, which would meaningfully de-risk the group's profitability profile.

The Vertical Integration Advantage

The most important number in the VGL story is 63%, the gross margin that the company has consistently defended even as the broader retail world grappled with inflation, supply chain disruption, and consumer downtrading.

To appreciate how unusual this is, consider that a typical fast fashion retailer earns 50–55% gross margins, a mass-market jewellery retailer typically earns 40–50%, and a branded consumer goods company would celebrate 60%+ margins as a signal of pricing power. VGL earns 63% while selling affordable jewellery in the $25–$50 range to middle-income consumers in Western markets. The reason is structural: when you own everything from production to customer, the margin that would otherwise be shared across four to five entities in the supply chain stays with you.

Looking at the trend over five years, gross margins have been remarkably stable, consistently in the 60-63% band even through the FY23 trough year. The FY23 period was unusual: it was the year that the pandemic-era demand boom in home shopping unwound sharply, revenues fell from ₹2,752 crore in FY22 to ₹2,491 crore in FY23, and net profit collapsed from ₹237 crore to ₹105 crore. Gross margins held. The business model proved its resilience not in the good years, but in that bad one.

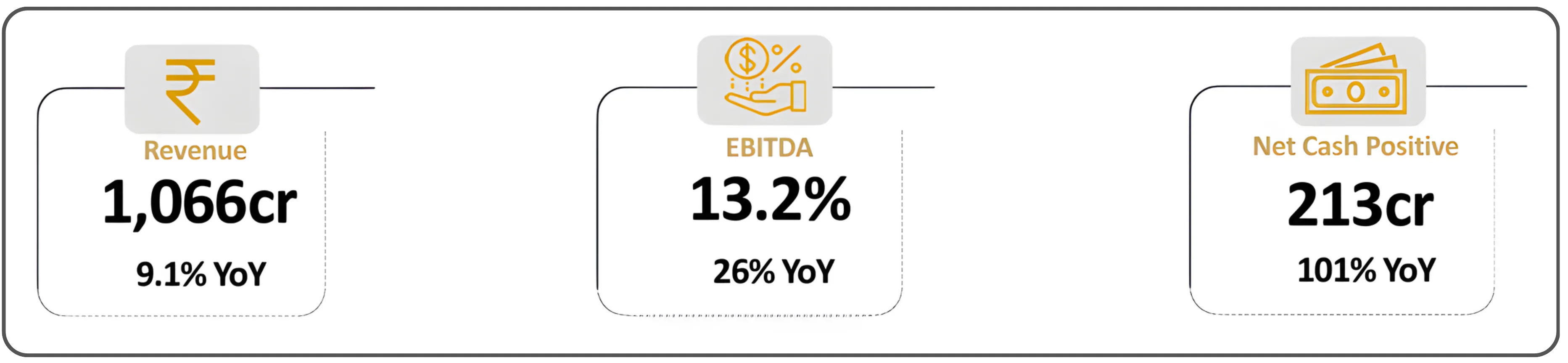

By Q3 FY26, the margin recovery has been comprehensive. EBITDA margins expanded 170 basis points year-on-year to 13.2%, driven by 120 basis points of employee cost improvement, 60 basis points of airtime cost leverage, and better product mix, partially offset by intentional investment in digital marketing. Management has explicitly guided for EBITDA margins of 10.5–11% for FY27 on a full-year basis, with room to expand further as operating leverage compounds.

The Revenue Journey

The sales trajectory of VGL over the past decade illustrates a business that had a COVID-fuelled boom, a painful normalization, and is now back on a sustainable growth path.

| Year | Revenue (₹ Cr) | Net Profit (₹ Cr) | OPM |

|---|---|---|---|

| FY20 | 1,986 | 190 | 13% |

| FY21 | 2,540 | 272 | 15% |

| FY22 | 2,752 | 237 | 10% |

| FY23 | 2,491 | 105 | 7% |

| FY24 | 3,041 | 127 | 9% |

| FY25 | 3,380 | 153 | 9% |

| TTM (Q3 FY26) | 3,607 | 209 | 9% |

The FY21–FY22 surge was real but transitory, Western consumers stuck at home discovered TV and digital shopping, and VGL rode that wave. The FY23 correction was sharp. What matters for the investment thesis is what happened next. Revenue has grown from ₹2,491 crore in FY23 to ₹3,607 crore on a trailing twelve-month basis (a 45% recovery) while net profit has more than doubled from ₹105 crore to ₹209 crore. This is not a business limping back to health. It is one where the operating leverage is beginning to kick in.

In Q3 FY26, the company crossed ₹1,000 crore in quarterly revenue for the very first time, with the management describing it as "slightly ahead of our guidance." PAT for the quarter came in at ₹90 crore, growing 41% year-on-year.

Vaibhav Global's supply chain is built in Jaipur and sold in three continents. Understanding how India's logistics sector makes that possible is worth reading next. A Comprehensive Analysis of India's Logistics and Supply Chain Sector — Part 1/2

The Digital Transition

The most consequential strategic shift happening inside VGL right now is the migration from TV-led to digitally-led revenue. In FY20, digital accounted for 33% of B2C revenue. It is now at 42% and heading to a stated target of 50% by FY27.

This matters because the economics of digital and TV customers are fundamentally different. TV customer acquisition is expensive; you bid for airtime slots, broadcast to a broad audience, and convert a fraction. Digital allows for targeted acquisition through paid social, search, and OTT platforms, with the ability to measure and optimize customer lifetime value precisely. As MD Sunil Agrawal noted in the Q3 FY26 call, "the lifetime value of an OTT customer is much higher than a TV customer."

The company has deliberately moved away from low-ticket, high-volume digital customer acquisition, pulling back from the $10–$30 price point on platforms and leaning into higher average selling price cohorts. This has suppressed unique customer count growth (up just 2% year-on-year in TTM Dec-25), but has improved customer profitability. The CFO described it plainly: the company is optimizing for customer quality, not customer quantity.

Lab-grown diamonds are an emerging driver within this shift. LGD now accounts for approximately 10.7% of retail revenue at an average selling price of $250 per piece, significantly above the overall portfolio average. The adoption is accelerating on both TV and digital, and management sees it as a structural product category, not a trend.

The Own-Brand Strategy

For most of its history, VGL sold products, often of excellent quality, always at value prices. What it did not do convincingly was build brands. That is changing. The company has built a portfolio of 16 in-house brands spanning categories and markets, including names like Rhapsody (premium gemstone jewellery), Iliana (18K gold), Homesmart, and Evertrue. In Q3 FY26, in-house brands contributed 48% of gross B2C revenue. The target is 50% before FY27.

Why does this matter? Brand revenue generates superior customer retention, higher repeat purchase rates, and pricing power that commodity product assortments cannot sustain. Every additional percentage point of in-house brand revenue is a shift toward a stickier, more margin-accretive revenue base. The Rachel Galley D2C brand is an early proof of concept launched as a small pure-digital brand four years ago, it tripled revenues within a recent quarter after the company cracked the right product-channel-price combination. The playbook is now being replicated across other brands.

The Acquisitions

Two acquisitions define VGL's inorganic strategy, and both are instructive. Ideal World, a UK general merchandise TV shopping channel, was acquired for ₹12 crore in September 2023. On a trailing twelve-month basis, it now generates £28–30 million in annual revenue (approximately ₹300+ crore), has 142,000 unique customers, and is profitable at EBITDA margins comparable to TJC. The acquisition cost was trivial relative to the revenue and channel footprint obtained. It has since been integrated into VGL's supply chain, allowing cross-selling of VGL's jewellery and lifestyle inventory through an additional broadcast channel.

Mindful Souls, a wellness and lifestyle D2C brand acquired for ₹105 crore, operates as a subscription and e-commerce business with 106,000 unique customers, 75%+ gross margins, and improving unit economics. It is the company's clearest signal of intent in the lifestyle and digital-first space.

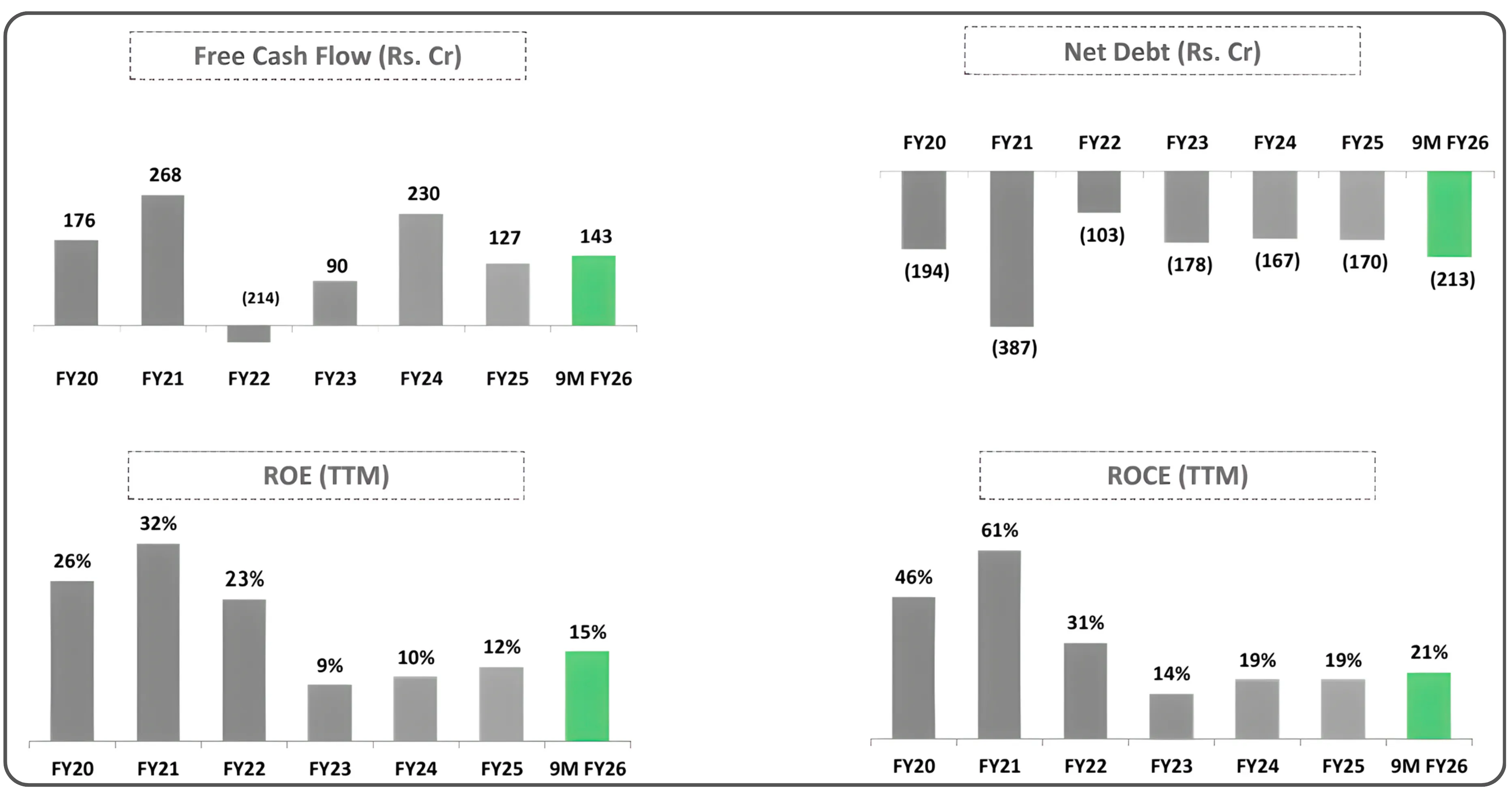

Together, these two acquisitions cost ₹117 crore and materially added to VGL's channel footprint, customer base, and profitability, without straining the balance sheet. For context, VGL generated ₹143 crore of free cash flow in 9M FY26 alone.

The Capital Returns Story

ROCE tells the story most clearly. In FY20, VGL earned 19% ROCE on capital employed. The COVID boom temporarily inflated returns to 46% in FY21. The normalization sent ROCE to 9% in FY23. And since then, the recovery has been disciplined and steady: 19% in FY24, 19% in FY25, 21% in 9M FY26. The company is generating these returns on a net-cash-positive balance sheet, ₹213 crore in net cash as of Q3 FY26. There is no financial leverage amplifying these returns artificially.

| Year | ROCE | ROE | Free Cash Flow (₹ Cr) |

|---|---|---|---|

| FY20 | 19% | 32% | 90 |

| FY21 | 46% | 61% | 230 |

| FY22 | 31% | 26% | 268 |

| FY23 | 9% | 12% | 127 |

| FY24 | 19% | 10% | 176 |

| FY25 | 19% | 14% | 143 |

| 9M FY26 | 21% | 15% | 143* |

On capital returned to shareholders, the picture is consistent. VGL has paid three interim dividends in FY26 of ₹1.5 per share each. In FY25, the total dividend payout ratio was approximately 78% of earnings. The balance sheet discipline is evident: even after paying out the majority of earnings as dividends and funding two acquisitions, the company has built (not depleted) its net cash position. Operating cash flow in Q3 FY26 stood at ₹160 crore, growing 105% year-on-year.

Every product VGL ships across three western markets starts with packaging. Here is how that industry works in India. The Packaging Industry in India — Structure, End-Use Demand, and Industry Dynamics

What the Market Is Pricing In

At the current market price of ₹240 (as of February 19, 2026), VGL trades at the following multiples:

| Metric | Value |

|---|---|

| Market Cap | ₹4,008 Cr |

| Stock P/E | 19.1x |

| EV/EBITDA | 11.0x |

| Price to Sales | 1.11x |

| ROCE | 14.0% |

| 52-Week Range | ₹178 – ₹293 |

The median EV/EBITDA multiple over the past five years is approximately 22x, which implies the current 11x is at a deep discount to its own history. At the guidance midpoint of 10.75% EBITDA margin on FY27 revenue of approximately ₹3,800 crore, EBITDA would be roughly ₹410 crore. Applying even 14x (a conservative multiple for a company with 20%+ ROCE, net cash, and growing free cash flow) implies a valuation significantly above current levels.

The P/E at 19.1x looks optically reasonable, but it is based on a trailing earnings base that has been suppressed by heavy digital investment and the Germany drag. Both of those are now reversing; Germany turned profitable in Q3 FY26, and digital marketing spend is beginning to show measurable returns. The earnings trajectory for FY27 is northward.

At 1.11x price-to-sales on a capital-light, 63%-gross-margin business generating consistent free cash flow, the market appears to be pricing VGL at a consumer commodities multiple rather than the quality retailer multiple it arguably deserves.

The Risks

Consumer spending sensitivity in core markets

The US and UK together contribute the bulk of VGL’s revenue. Both markets are dealing with high interest rates, rising housing costs, and softer discretionary spending. This directly affects demand for non-essential purchases. Management has also highlighted elevated precious metal prices as a headwind in these regions. Importantly, FY27 guidance has been framed without assuming any recovery in consumer sentiment. If spending improves, the outlook may prove conservative. If conditions worsen, earnings could come under pressure.

Declining TV viewership and the shift to digital

Linear TV audiences in Western markets continue to decline as viewers move away from cable and satellite services. This is a long-term structural shift. VGL is responding by accelerating its digital and OTT presence, which aligns with changing consumption habits. However, this transition brings higher content and broadcasting costs. Management has indicated that digital content spending will continue as a strategic investment and is unlikely to benefit from operating leverage, which may limit EBITDA margin expansion.

Currency exposure

VGL earns most of its revenue in USD and GBP while a large portion of its costs are in INR. This provides a natural hedge, as a weaker rupee supports profitability. A stable or strengthening rupee would have the opposite effect. The company has not shared detailed hedging practices in earnings calls, leaving limited visibility into how this risk is managed.

What Unlocks the Value

Three developments, if they materialize in FY27, could meaningfully close the gap between where VGL trades and where its fundamentals point.

The most immediate catalyst is German profitability. Germany has been burning money since its launch, a drag on consolidated profitability that the market has penalized. Having turned segment-EBITDA-positive in Q3 FY26, and with management guiding for full-year EBITDA profitability in FY27, the Germany narrative is flipping from "cost centre" to "growth market." The total addressable market in Germany alone is estimated at $3 billion. VGL has only just scratched the surface.

The second is operating leverage at the group level. Revenue guidance is 9–11% growth in FY27 on a base of ₹3,380 crore, implying ₹3,700–3,750 crore. The fixed cost base (TV airtime, warehousing, technology) does not scale proportionally. Employee costs (the largest variable) are being optimized partly through AI and process change. If EBITDA margins approach the management-guided 10.5–11%, that represents 150–200 basis points of expansion on the current run-rate, and a PAT in the range of ₹250–280 crore on a full-year basis.

Ongoing India–EU Free Trade Agreement negotiations are expected to include a 4% duty benefit on jewellery exports from India to Germany. If implemented, this would directly benefit manufacturers like Vaibhav Global that export from Jaipur into European markets.

Conclusive Take on Vaibhav Global

Vaibhav Global is a genuinely unusual business. It solved a hard problem, how do you sell affordable, quality jewellery to middle-income Western consumers at scale without paying for shelf space; by building its own shelves: proprietary TV channels beaming into 127 million homes, and digital platforms that are quietly becoming the dominant channel.

The numbers tell a story of a business with structural advantages: 63% gross margins, improving ROCE (9% trough to 21% today), consistent free cash flow generation, and a net-cash balance sheet. The FY23 trough was real and painful, but it revealed something important, the gross margin moat did not break. The business held its structural advantage through the worst of it.

Digital is growing at 16% CAGR over five years and has just crossed 42% of revenue; Germany has just turned profitable and the acquisition of Ideal World for ₹12 crore has already yielded a fully profitable, 142,000-customer UK channel. The question for investors is not whether VGL is a great business, the margins and return ratios answer that. The question is whether the market's pessimism about the transition speed is justified.

Turn research into action, trade smarter on CubePlus.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.