Fixed deposits (FDs) and the Public Provident Fund (PPF) are two of the safest investment options available to Indian investors seeking steady, long-term returns. Both instruments serve distinct purposes and deserve careful comparison before you decide where to invest your money. Whether you are focused on tax saving investments India or building a retirement corpus, understanding both options is key.

With an FD, you park a lump sum with a bank or financial institution for a set duration at a predetermined interest rate typically earning more than a regular savings account would offer. PPF, on the other hand, is a government-backed savings scheme introduced in 1968 that offers tax-free interest and is built for wealth creation over the long haul.

Also Read: 9 Smart Money Moves for 2026

Fixed Deposit

FDs work particularly well when you are saving towards something specific. They cannot be automated. If you want monthly investing, a Recurring Deposit (RD) may be more suitable. Once FD tenure ends, anywhere between 7 days and 10 years, you can either withdraw the principal along with interest or roll it into a fresh FD if the prevailing rates suit you.

Check Tradejini’s FD Calculator

You can also set up separate FDs for different milestones such as a child's education, school fees, a wedding, or a planned holiday. Interest rates tend to be more attractive on medium to longer tenures, though they generally soften beyond the three-year mark. Senior citizens aged 60 and above usually receive a slightly better rate than regular depositors across most banks. Currently, annual FD rates across Indian banks range between 5.5% and 7.75%.

Also Read: PPF Explained

Public Provident Fund

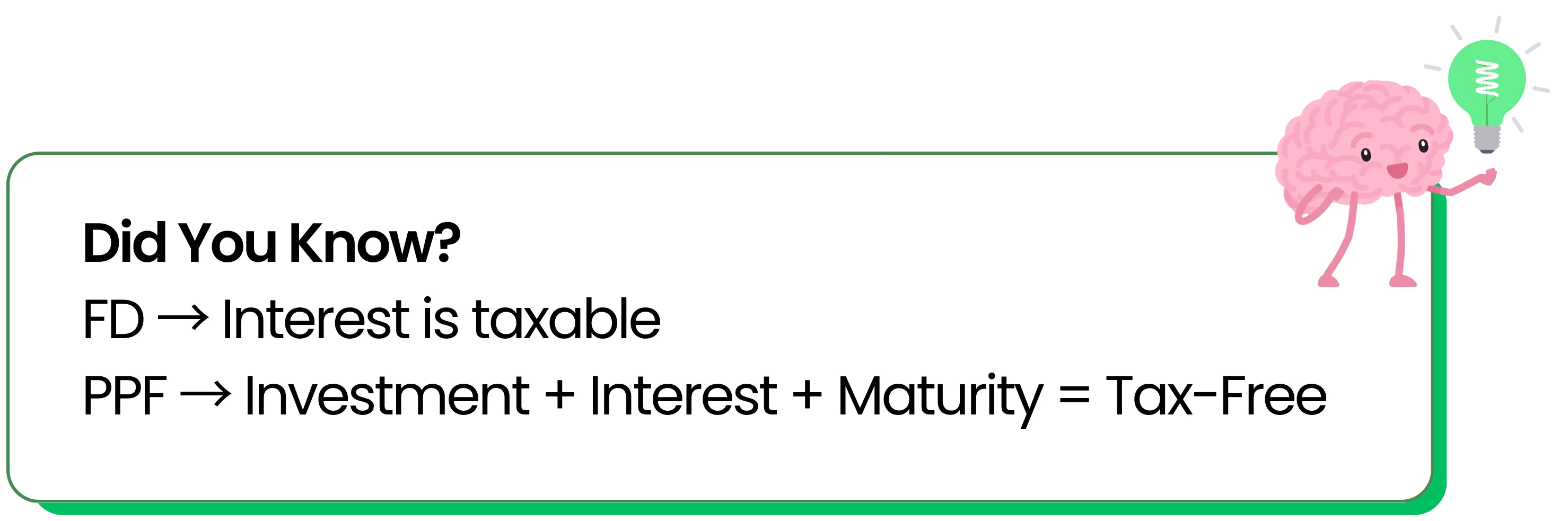

PPF is a government-guaranteed scheme that comes with a rare triple tax exemption: your investment, the interest you earn, and the final maturity amount are all tax-free. The PPF interest rate 2025 currently stands at 7.1% per annum and is considered one of the most reliable vehicles for retirement planning India.

Check Tradejini’s PPF Calculator

You can open a PPF account at any post office, public sector bank, or select private banks, minimum annual contribution is ₹500, and maximum is ₹1.5 lakh. Opening an account requires standard KYC documents, an Aadhaar card, proof of address, and a passport-size photo and can also be done conveniently through your bank's online or mobile banking platform.

| Fixed Deposit | Public Provident Fund |

|---|---|

| Tax-saving FDs come with a 5-year lock-in period. | The minimum tenure is 15 years and can be extended in blocks. |

| Residents of India, corporates, HUFs, trusts, and NRIs can open an FD account. | Only resident Indian individuals can open a PPF account. |

| There is no maximum investment limit. | Maximum investment allowed is ₹1.5 lakh per financial year. |

| Interest rates typically range between 5.5% and 7.75% depending on the bank and tenure. | Current interest rate is 7.1% per annum. |

| Loan facility is available against FD. | Loan facility is available only after the 3rd financial year. |

When Should You Choose FD vs PPF?

If your goal is short-term stability or you may need access to your money, a Fixed Deposit works better. It offers flexibility in tenure and relatively easy liquidity, making it suitable for planned expenses or parking surplus funds.

On the other hand, if you are building a long-term corpus, especially for retirement, PPF is more suitable. The 15-year lock-in may feel restrictive, but it enforces discipline and allows your money to compound tax-free over time.

Liquidity and Risk Perspective

Both FD and PPF are considered safe instruments, but they differ significantly in terms of access to funds. Fixed Deposits are relatively liquid. You can withdraw prematurely, although it may come with a small penalty. This makes FDs useful when flexibility matters.

PPF, in contrast, is designed for long-term commitment. Partial withdrawals are allowed only after a few years, and full withdrawal is possible only at maturity. This lack of liquidity is not a drawback if your goal is disciplined, long-term savings.

Conclusion:

Choose FD if you:

- Need flexibility and may require access to your money before a fixed deadline

- Are saving for a specific short- to medium-term goal like a vacation, wedding, or school fees

- Are a senior citizen looking to earn a slightly higher, predictable return

- Are a corporate, HUF, trust, or NRI who cannot open a PPF account

Choose PPF if you:

- Are building a long-term retirement corpus and can stay invested for 15+ years

- Fall in a higher income tax bracket and want to maximise your tax savings

- Prefer a government-guaranteed instrument with zero credit risk

- Want your returns to be completely tax-free at maturity

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.