Imagine you waking up one morning to realize that despite years of investing in random mutual funds, your money is scattered everywhere but isn’t moving you closer to any real goal. This is exactly where most investors get stuck, not because they don’t invest, but because they don’t know how to build a mutual fund portfolio construction.

So, let's cut through the clutter and learn how to build a mutual fund portfolio that actually works for your life goals.

Step 1 – Get the basics right

Before you even think of investing in mutual funds, you need to have two essentials in place:

Risk cover

This comes through insurance. Life is uncertain, and risks can come in many forms, such as health issues, job loss, or even personal setbacks. While you cannot protect yourself from everything, two things are non-negotiable:

- A term insurance plan to secure your family financially in case of your absence.

- A health insurance plan to handle hospitalization expenses.

Emergency Corpus

Life throws surprises in the form of sudden job loss, medical needs, or unexpected big-ticket expenses. That’s why having an emergency fund that is liquid and accessible is critical.

While the common rule is to set aside six months’ worth of expenses, the right amount should really depend on your family’s unique circumstances.

Also Read:

How to Start SIP: A Guide on Mutual Funds Online & How Mutual Fund Payments Work

Step 2 – Define Your Financial Goal

A portfolio should not be random, it should be built to serve a specific financial goal. A financial goal must have three clear attributes:

- The amount of money required.

- The time horizon for achieving it.

- The current age and profile of the investor.

For example:

A couple in their late 20s planning to buy a ₹1.5 crore house in 10 years.

A 40-year-old parent aiming to save ₹25 lakh in 8 years for their child’s education abroad.

A 21-year-old professional saving ₹20 lakh in 8 years for higher studies.

It can be the best mutual fund portfolio for 10 years, but without clarity on these details, your goals remain vague, and so will your portfolio. Additionally, mutual fund portfolio allocation by age is vital.

Step 3 – Use a portfolio template

| Fund Type | Category | Expected CAGR | Minimum Holding | Suitable For | Key Remark |

|---|---|---|---|---|---|

| Large Cap | Equity | 10–12% | 7+ years | Long-term wealth, big-ticket goals | Stable, less volatile than mid/small cap |

| Mid Cap | Equity | 12–14% | 7+ years | Growth-focused long-term goals | Volatile, needs discipline |

| Hybrid | Mix | 8–10% | 5+ years | Medium-term goals | Balanced risk |

| Debt – Short Duration | Debt | 6–7% | 3+ years | Medium-term, predictable goals | Safer than equity |

| Arbitrage | Hybrid | 6–7% | 3+ years | Short-to-medium term | Tax-efficient, low risk |

| Liquid Fund | Debt | 4–5% | Anytime | Emergency corpus | High liquidity |

Step 4 – Avoid redundancy

Many investors end up with 10–12 overlapping funds (multiple large caps, multiple mid caps, and so on).

This creates a messy, directionless portfolio. Ideally, stick to a handful of funds that complement each other and align with your financial goal.

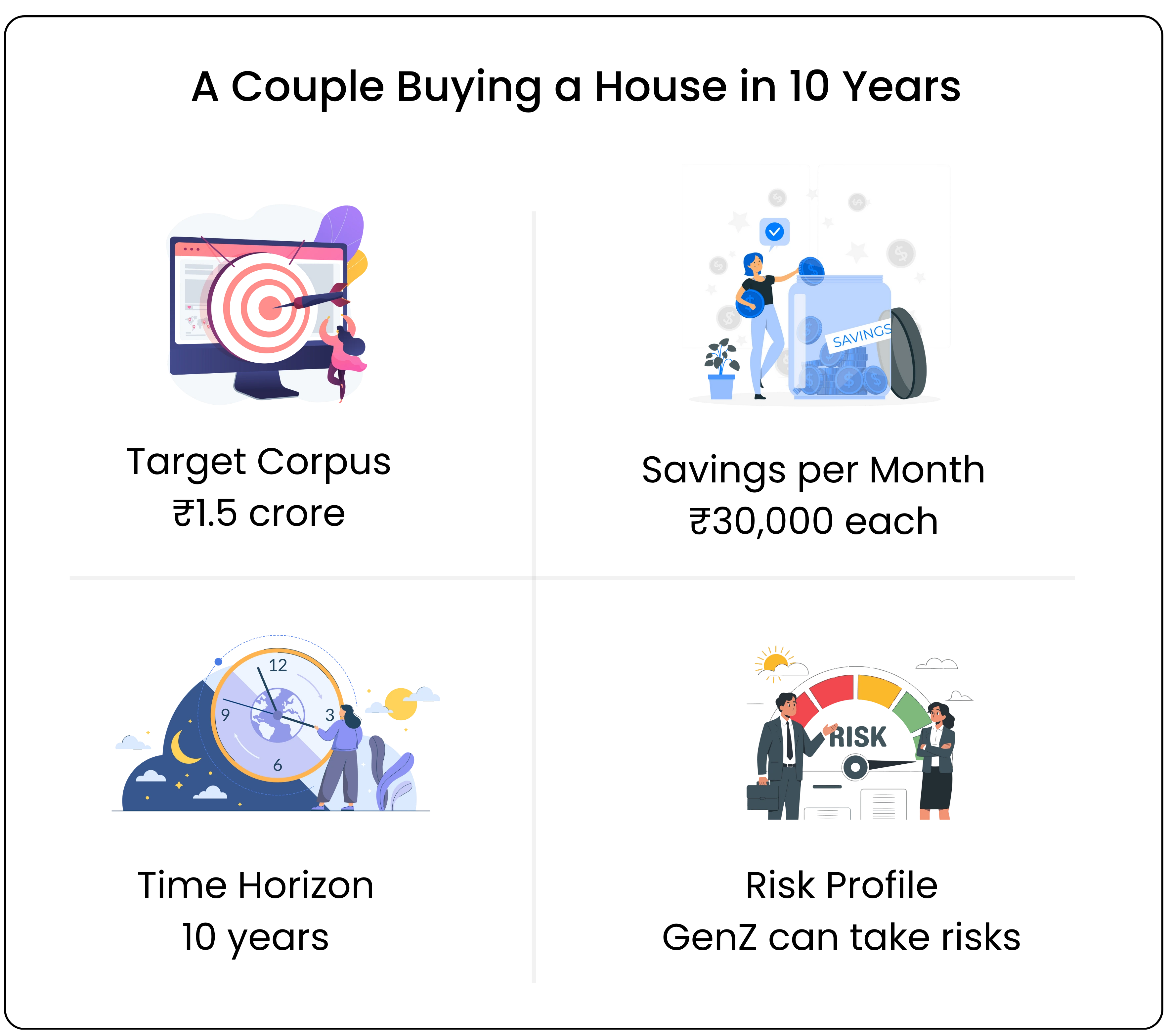

Example 1 – A Couple Buying a House in 10 Years

- Target Corpus: ₹1.5 crore

- Savings per Month: ₹30,000 each

- Time Horizon: 10 years

- Risk Profile: GenZ can take risks

Also Read: Planning to Invest in Mutual Funds? Start With These 9 Steps

Portfolio approach:

- Avoid short-term debt, small-cap, thematic, and focused funds due to their higher volatility and concentration risk.

- Stick to one Large Cap Fund and one Mid Cap Fund (one each).

- Invest via SIP investing for beginners for disciplined compounding.

Outcome:

At ~10% expected CAGR from mutual funds, they can accumulate around ₹1.2 crore. The remaining shortfall can be bridged via a bank loan. To safeguard gains, they should shift to debt funds before goal around the 8th year.

Example 2 – Parent saving for child’s overseas education

- Target Corpus: ₹25 lakh

- Monthly Investment: ₹20,000

- Time Horizon: 8 years

- Risk Profile: Moderate

Portfolio approach:

- Debt should play a bigger role since the horizon is below 10 years.

- Ignore liquid/overnight funds and credit risk funds.

- Use a Short Duration Debt Fund or Corporate Bond Fund, along with a Hybrid Fund or Arbitrage Fund.

- Optionally, allocate 20–25% to a Large Cap Fund for growth.

At ~7% CAGR, the goal is achievable within the timeline.

So, what investors need to do

- Be conservative in return assumptions – If actual returns exceed your estimates, consider it a bonus.

- Remember equity is lumpy – Unlike fixed deposits, equity returns don’t come evenly, they arrive in bursts and corrections. This is why disciplined SIP investing with patience is the best strategy.

- Protect your capital near goal year – Start shifting to debt funds gradually as you approach your target date to safeguard your gains.

Building a mutual fund portfolio is about balancing risk, time, and goals, not about chasing returns blindly.

Following this approach ensures your mutual fund portfolio for financial goals is structured, disciplined, and purposeful.

Curious how your SIP grows monthly? Try Tradejini’s calculator.