Whenever you invest in mutual funds, returns are only one part of the story. Taxes play an equally important role in deciding what finally reaches your bank account. In the Union Budget 2025, the government has reshaped how long-term capital gains from mutual funds are taxed, and these changes apply from FY 2025–26 onwards.

For investments made on or after 1 April 2023, gains from debt mutual funds are taxed at the investor’s applicable income tax slab rate, irrespective of the holding period. No indexation benefit is available on these investments.

This change simplifies the tax structure but also alters how investors should look at post-tax returns.

How Mutual Funds Are Classified for Taxation

For tax purposes, mutual funds are broadly divided into two categories. This classification decides both the holding period and the tax treatment.

Equity-oriented mutual funds

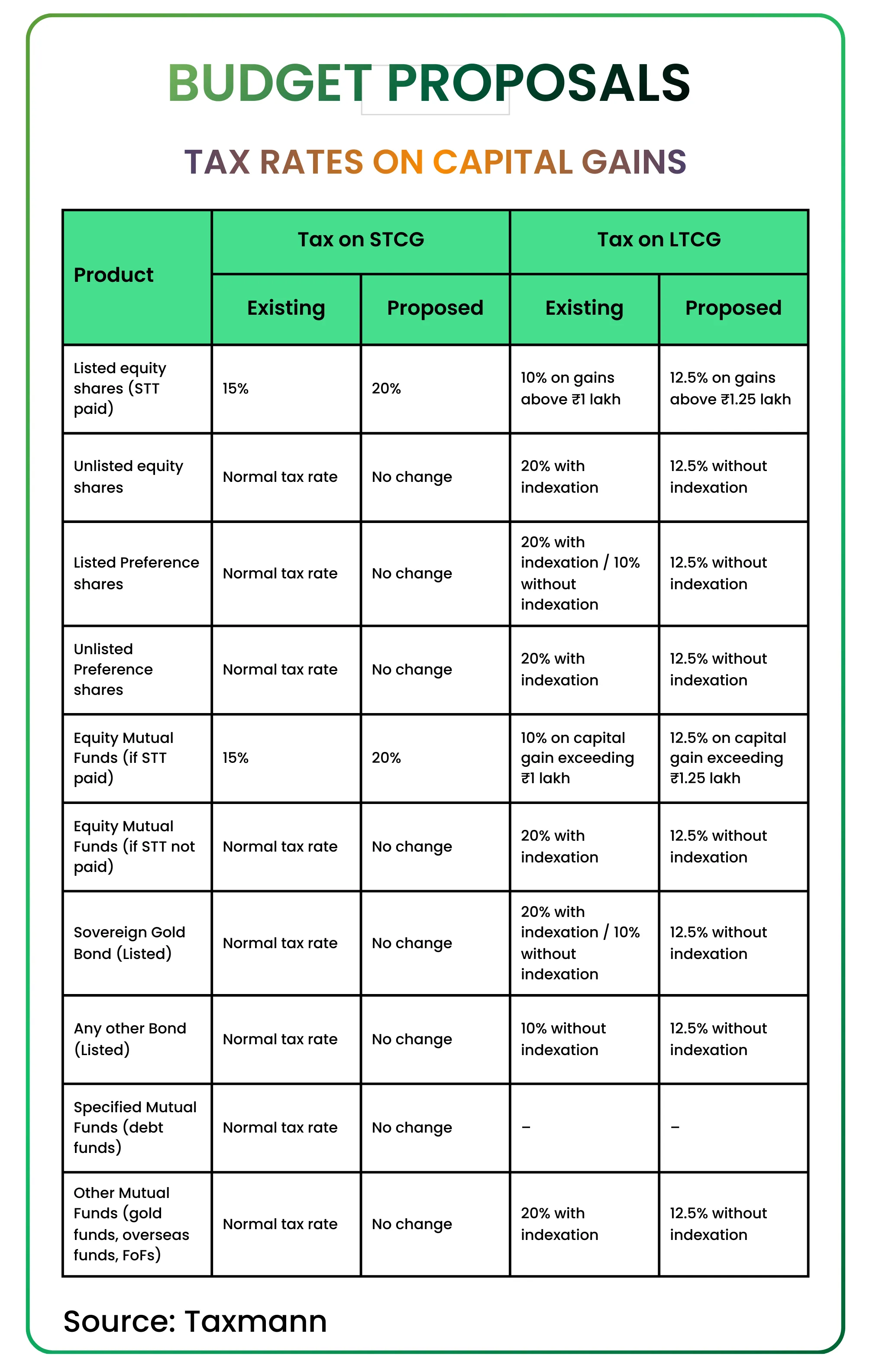

Long-term capital gains from equity-oriented mutual funds are taxed at 12.5 percent, along with applicable surcharge and 4 percent cess, on gains exceeding ₹1.25 lakh in a financial year. To qualify as long-term, the units must be held for more than 12 months.

Debt-oriented mutual funds

These funds invest in instruments like bonds, treasury bills, government securities, and corporate debt. Under the latest tax rules, debt mutual funds no longer qualify for long-term capital gains. Gains from debt mutual funds are treated as short-term capital gains and are taxed as per the investor’s applicable income tax slab rate.

Long-Term Capital Gains Tax Rates

Under the revised rules:

Long-term gains from equity-oriented mutual funds are taxed at 12.5% + applicable surcharge + 4% cess on gains exceeding the ₹1.25 lakh annual exemption limit.

For units purchased before 1 April 2023, transitional provisions apply. However, if such units are sold on or after 23 July 2024, long-term capital gains are taxed at 12.5 percent without indexation under the current framework.

If the units were acquired on or after 1 April 2023, there is no preferential LTCG rate, gains are treated as short-term and are taxed at the investor’s income tax slab rate.

Earlier, debt funds attracted a higher tax rate with indexation benefits. The new framework removes this distinction and applies a flat rate without indexation.

Exemptions and Tax Relief Available

Even though the tax rate has been streamlined, certain exemptions still help reduce the tax burden.

The ₹1.25 lakh annual exemption applies only to long-term capital gains arising from equity-oriented mutual funds and listed equity shares. It does not apply to debt mutual funds.

Why This Matters for Investors

Understanding how long-term capital gains tax works is essential for planning mutual fund investments effectively. Post-tax returns can differ significantly from headline returns, especially for long-term debt investors after the removal of indexation.

As always, investment decisions should factor in time horizon, risk, returns, and taxes, not just past performance.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.