When investing in mutual funds, the investment returns you earn are not only determined by fund performance in the market but also by the expenses involved in managing it. These mutual fund charges, though often overlooked, can significantly affect your long-term investment returns and investment decisions. To make informed investment decisions, it’s essential to understand how these expenses are measured and what they mean for your portfolio.

Let's examine the three key measures that reveal a mutual fund's cost efficiency – how fund companies structure costs and what investors pay:

Portfolio Turnover Ratio, Expense Ratio, and Entry/Exit Load.

Portfolio Turnover Ratio

The Portfolio Turnover Ratio (PTR) measures how frequently a fund manager buys and sells securities within the fund’s portfolio during a year. It shows the level of trading activity and helps investors assess how actively a fund is being managed.

For instance, suppose a mutual fund investments have ₹200 crore in fund assets and sells securities worth ₹40 crore during the year. The Portfolio Turnover Ratio would be:

40 ÷ 200 = 20%

This means 20% of the portfolio was replaced during the year.

If the fund assets rise to ₹250 crore and the fund manager decides to replace the entire portfolio in actively managed mutual funds once, the turnover ratio becomes 100%. If they do this twice in a year, the ratio would be 200%, meaning the portfolio was completely churned every six months.

Typically, liquid and money market funds tend to have higher portfolio turnover ratios compared to index funds and exchange-traded funds because the underlying securities have short maturities. As fixed income securities mature, fund managers must reinvest in new instruments, leading to frequent churn in debt funds.

However, a higher turnover ratio in actively managed funds also implies higher transaction costs and brokerage fees, which can eat into returns over time.

Want to know how our intern managed her first stipend? Read her story here:

Spent or Saved? What I Did with My First Stipend

Expense Ratio

The Expense Ratio indicates the percentage of a fund’s average net assets that go toward covering annual operating expenses. These annual expenses that many mutual funds charge include:

- Investment management and advisory fees charged by the AMC

- Marketing expenses and distribution costs that fund companies incur

- Brokerage fees and transaction costs excluding fund portfolio management

- Administrative expenses, administrative fees, and account fees regulated by Securities and Exchange Board

In short, it measures the operational cost of fund management expressed as a percentage.

For example, if a mutual fund has average assets of ₹500 crore and annual expenses of ₹7.5 crore, the expense ratio would be:

(7.5 ÷ 500) × 100 = 1.5%

This means ₹1.5 is deducted annually for every ₹100 of assets under management to cover fund management costs.

Expense ratios vary across fund types. Equity funds typically have higher expense ratios (around 1.5%–2%) than debt funds, which are often below 1%.

While a lower expense ratio is generally better for investment returns, it's equally important to consider fund performance and investment strategy. Sometimes, funds with slightly higher expenses deliver better risk-adjusted due to skilled management.

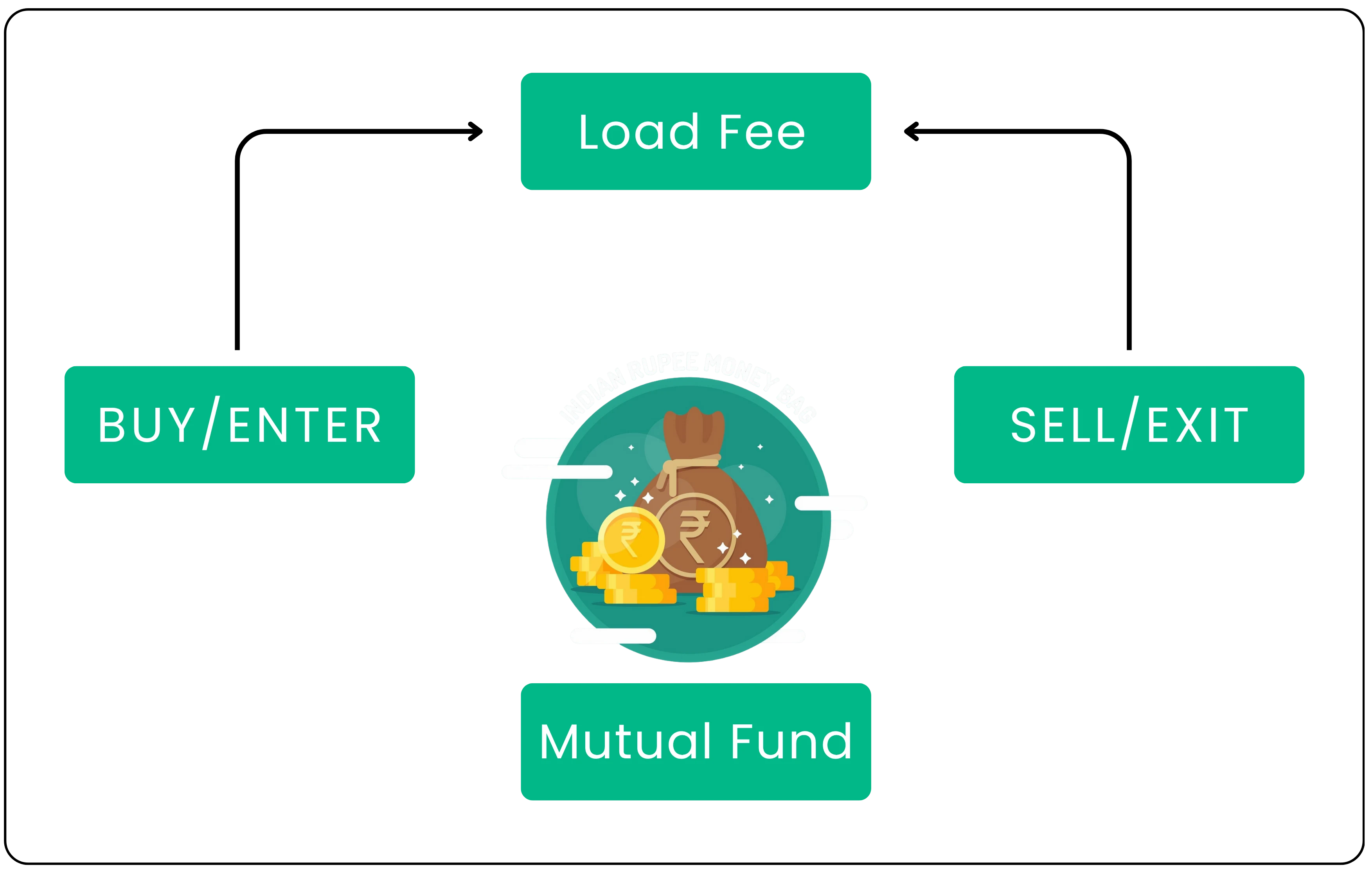

Entry and Exit Load

A Load is a mutual fund charge and redemption fee that funds impose when an investor purchases shares or when selling fund shares. It compensates the fund house for distribution expenses, distribution fees, and administrative costs.

- Entry Load: Charged when you buy mutual fund units (entry load on mutual funds is banned in India by SEBI).

- Exit Load: Charged as a redemption fee when you redeem your investment within a specified period, usually to discourage short-term trading.

Let’s understand with an example.

Now, assume you sell these units when the NAV is ₹30 and the exit load is 0.5%.

The redemption price per unit = ₹30 - (0.5% of 30) = ₹29.85

Your redemption amount = 792.08 × 29.85 = ₹23,642.79

So, while your mutual fund investments gained value, the mutual fund charges slightly reduced your total investment returns.

Mutual funds that don't levy these charges are called 'No Load Funds', offering better overall expense ratio.

The Real Cost

Even small differences in the total expense ratio and mutual fund fees can compound significantly over time, affecting assets under management returns. As an investor making investment decisions, it's important to look beyond investment returns and understand how efficiently your money is managed through professional money management.

Mutual fund schemes with reasonable costs, disciplined fund management, and consistent fund performance can create far greater long-term value, whether equity funds or growth funds than actively managed mutual funds with higher churn, higher expense ratio, and hidden costs incurred.

Before investing in mutual funds, always review the expense ratio, turnover ratio, exit load, and understand regular and direct plans differences in the fund house factsheet. These details about mutual fund charges and the fee paid often make a big difference in your investment returns and tax implications.

Ready to explore further? Our detailed Mutual Fund Guide walks you through the process step by step: Mutual Funds User Guide

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.