Mutual fund returns often look impressive on paper. A fund reports 15% yearly returns over ten years, and most people naturally assume their own money must have grown at the same pace. But when investors finally calculate what they actually earned, the number is usually much lower. Sometimes a little lower. Sometimes shockingly lower.

This gap between what funds show and what investors experience is not a calculation error. It is not a hidden fee problem. It is not because fund managers are secretly bad at their jobs. It happens mainly because of investor behavior.

In simple words, people invest at the wrong times.

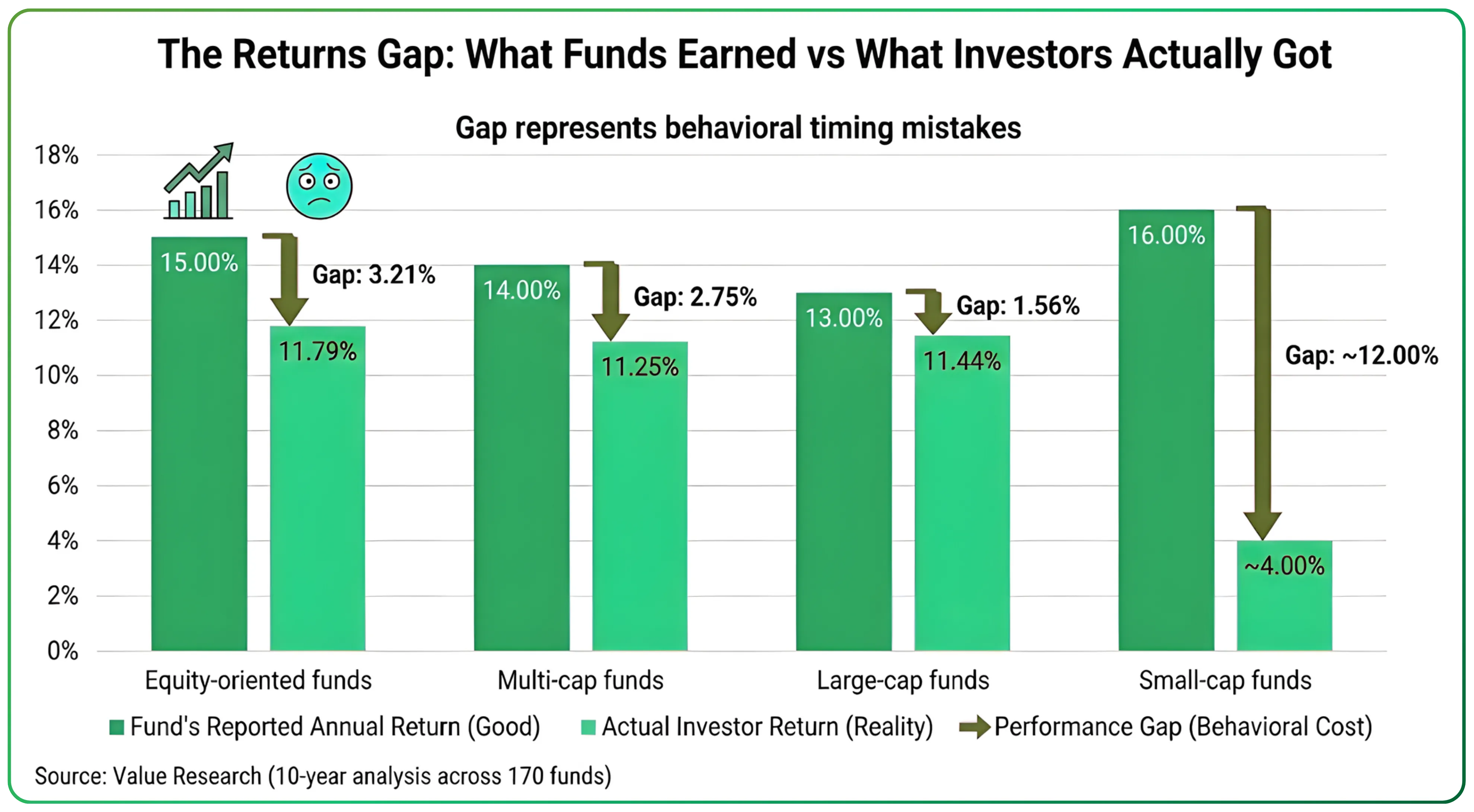

A recent study by Value Research measured this gap across 170 diversified equity mutual funds over ten years. The results were uncomfortable. While the funds delivered strong long-term performance, the real returns earned by investors were consistently lower.

In equity-oriented funds, investors earned about 3.21% less every year than the fund returns. In multi-cap funds, the gap was around 2.75% per year. Even large-cap funds, which most people consider stable and safe, showed a 1.56% yearly shortfall. Small-cap funds were the worst. Over ten years, investors in small-cap funds earned nearly 12% less than the funds themselves delivered.

These are not small differences. They do not cancel out over time. They quietly compound.

Over a decade, losing 3.21% every year means ending up with roughly 28% less money than someone who simply stayed invested from start to finish.

The funds did their job.

The damage happened because of how investors used them.

Timing Gap in Mutual Fund Returns vs Investor Returns

Mutual fund returns are calculated in a clean, ideal way. They assume that money was invested at the beginning and stayed invested the entire time. No panic. No excitement. No stopping. No restarting.

Investor returns are calculated using real cash flows. They track when money actually went into the fund and when it came out. They reflect real human behavior.

And real human behavior follows a very predictable pattern.

People invest more money when markets are rising and everything feels good. They reduce investments or withdraw money when markets are falling and fear takes over.

So most money enters when markets are expensive.

And most money leaves when markets are cheap.

This single habit explains most of the gap between mutual fund returns and investor returns in India.

What typically happens during market cycles

When markets are going up, headlines turn positive. New highs are celebrated. Friends talk about profits. Social media fills with screenshots of portfolios. SIP registrations increase. Mutual fund assets grow fast. More first-time investors enter the market.

But this enthusiasm usually comes after a large part of the market move has already happened. Prices are already high. Valuations are already stretched. Risk is already building quietly in the background.

People end up buying after the rally.

Then markets correct. News turns negative. Volatility rises. Red numbers spread across portfolios. The same people who proudly started SIPs during the rally now feel uneasy. Some pause their SIPs. Some withdraw money. Some exit completely.

Stepping away during market falls often feels like the safe decision. In reality, those moments usually arrive when prices are already lower and long-term return potential is improving. Many investors only realise this later. By then, they have already sold. The same pattern keeps repeating across years and across generations. Confidence peaks near market highs. Fear takes over after declines. Money flows in when comfort is high and flows out when discomfort rises. The behaviour sounds sensible and even responsible. Over long periods, it quietly does serious damage to wealth.

The emotional side of bad timing

This behavior is financially damaging, but psychologically natural.

Rising markets create confidence. They create excitement. They create fear of missing out. People feel foolish staying away when others seem to be making easy money.

Falling markets create discomfort. They create doubt. They create a strong urge to “protect whatever is left.” People feel smart stepping aside until things “become clear.”

Markets usually move long before things feel clear. When investing finally feels safe, prices have often already risen. When selling starts to feel necessary, much of the fall has already happened. Most decisions are not responses to real opportunity or real risk. They are responses to comfort and fear. By the time those feelings show up, the market has already moved on.

The Cost of Poor Timing and SIP Behavior Gap

The return gap sounds abstract until you convert it into money.

Imagine an investor starting a ₹10,000 monthly SIP in an equity fund that delivers 15% yearly returns over ten years. If they stay invested without stopping, they would build a corpus of around ₹27.5 lakh.

Now imagine the same investor, same fund, same market. But this time, they pause SIPs during market falls and restart them during rallies. Because of these timing decisions, their returns end up 3.21% lower each year.

After ten years, their corpus would be closer to ₹23.8 lakh.

That is a difference of ₹3.7 lakh.

On an investment of ₹12 lakh.

No wrong fund. No scam. No crisis.

Just behavior.

In volatile categories like small-cap funds, the damage has historically been much worse. Investors typically enter these funds after strong rallies, attracted by past performance. Then, when sharp corrections hit, they exit. Over ten years, this pattern alone caused investors to earn nearly 12% less than what the funds delivered.

Multi-cap and large-cap funds showed smaller gaps, but the story stayed the same. Even in the most stable categories, behavior reduced returns.

Because the problem is not product selection.

The problem is discipline.

Why investors struggle to behave well

Investors face a constant stream of information. Market news. Notifications. Daily NAV changes. Expert opinions. Social media noise. Portfolio apps that update in real time.

This constant stream of news and opinions makes patience very difficult. When everything around you sounds alarming, continuing to invest feels irresponsible. When optimism is everywhere, staying on the sidelines feels foolish. Most investors end up moving with the mood of the moment. The problem is that markets usually move before that mood changes. Prices shift first. Explanations follow later. When something finally feels attractive to everyone, it is often already expensive. When something finally feels dangerous to everyone, much of the fall has already happened. Decisions based on popular narratives usually arrive late. Over many market cycles, this delay has been one of the main reasons investor returns continue to trail fund returns.

The SIP behavior problem

SIPs were meant to make investing boring and automatic. The idea was simple. Money goes in every month, whether markets are rising, falling, or doing nothing. This steady flow removes the pressure of choosing the “right” time and naturally spreads purchases across different price levels. Over time, more units get picked up during weak markets and fewer during expensive ones.

In real life, most investors do not let SIPs run that way. They are treated as adjustable. When expenses increase, SIPs are among the first things to be cut. When markets turn volatile, contributions are slowed or stopped. When uncertainty shows up, discipline quietly disappears. Each pause seems reasonable in isolation. Together, they damage the very benefit SIPs were created for. Every skipped month often means missing lower prices. Every break in continuity pushes investor returns a little further away from fund returns.

What actually improves investor returns

Structural discipline is the solution to this problem.

First, SIPs must be treated as non-negotiable commitments. Like rent. Like insurance. Like loan EMIs. Something you do not skip just because the environment feels uncomfortable.

Second, portfolio watching must be reduced. Constant monitoring does not improve decisions. It increases emotional reactions. For long-term investors, quarterly reviews are more than enough. Daily or weekly checking mostly creates anxiety and overconfidence, depending on market direction.

Third, automation should be used aggressively. Manual investing leaves room for mood. Automation removes the decision moment where most mistakes happen.

Fourth, every investor needs a clear reason for investing. Long-term wealth. Children’s education. Financial independence. Retirement security. When markets fall, this reason matters more than market commentary.

Without a framework, every correction feels like a mistake. With a framework, corrections become part of the process.

The quiet power of doing nothing

One of the hardest lessons in investing is how powerful inaction can be. Investors who started SIPs years ago and then largely ignored them often ended up far better off than those who kept reacting to every market phase. They did not enter at perfect levels or escape every fall. They stayed invested through rallies, corrections, and long boring stretches in between. That continuity did more heavy lifting than any clever decision ever could. By remaining present through all conditions, they avoided most of the mistakes that activity creates. Over time, staying quietly invested solved problems that intelligence, timing, and constant monitoring rarely manage to solve.

The real issue behind low investor returns

If investing had no human emotions involved, the gap between fund returns and investor returns would shrink sharply. Markets repeatedly expose the same mental pressure points. Fear during falls. Confidence during rallies. Regret after missed moves. Social influence when everyone around seems to be making money. These forces quietly shape decisions. People feel safest entering when markets are already strong and most vulnerable exiting when conditions look worst. The result is a steady habit of increasing exposure as risk rises and cutting exposure just as future returns improve.

This is why booming SIP numbers during bull runs are not always a healthy sign. They often show that retail participation is peaking at stretched valuations. And this is also why slowing SIP flows during corrections are not always negative. They usually reflect fear, which has historically marked periods of better long-term opportunity. Mutual fund growth is real and meaningful, but a large part of that growth still arrives at the wrong stage of the cycle and for the wrong reasons.

The only commitment that matters

Long-term investing runs on routine, not foresight. Money grows when the habit continues through dull phases, falling markets, and long stretches when nobody is talking about stocks. These periods feel unproductive, even uncomfortable, which is exactly why most people struggle to stay invested. Many convince themselves that small timing changes will improve results. In reality, those changes usually follow mood, not logic. Fear creeps in during declines. Confidence swells after rallies. Decisions shift, and returns quietly slip. Over time, this repeated interference pulls investor outcomes below fund outcomes. The strategy itself rarely fails. What fails is the ability to leave it alone. Strong results come from staying put, not staying busy. In markets, discipline outlasts cleverness.

Start your investing journey today by signing up for CubePlus.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.