When the rupee weakens, conventional wisdom around Indian IT companies follows a predictable arc. Dollar-denominated revenues, when converted to rupees at a weaker exchange rate, expand the top line without any corresponding increase in business volume. For a sector earning the bulk of its revenue in foreign currency while incurring most of its costs domestically, this arithmetic has historically served as a reliable tailwind. In May 2026, with the rupee trading above 94 against the dollar the arithmetic is intact. Yet TCS, Infosys, HCL Technologies and Wipro are all trading within a narrow band of their respective 52-week lows. Reconciling this contradiction requires looking beyond currency movements and understanding the deeper drivers behind IT stock valuation in India. This is precisely why many investors are asking why Indian IT stocks are falling despite a weak rupee, even as the Nifty IT Index 2026 continues to underperform broader markets.

How Rupee Depreciation Affects IT Sector Earnings

Among the cleaner transmission mechanisms in Indian equity markets is the relationship between rupee depreciation and IT sector earnings. A company billing a client in dollars receives foreign currency that is subsequently converted to rupees at the prevailing exchange rate. When the rupee depreciates, the same volume of business yields more rupees, improving reported revenue and margins without any change in the underlying contract or service delivery. For a sector where roughly 85 to 90 percent of revenue is earned offshore, even modest depreciation can add several hundred basis points to earnings growth in rupee terms.

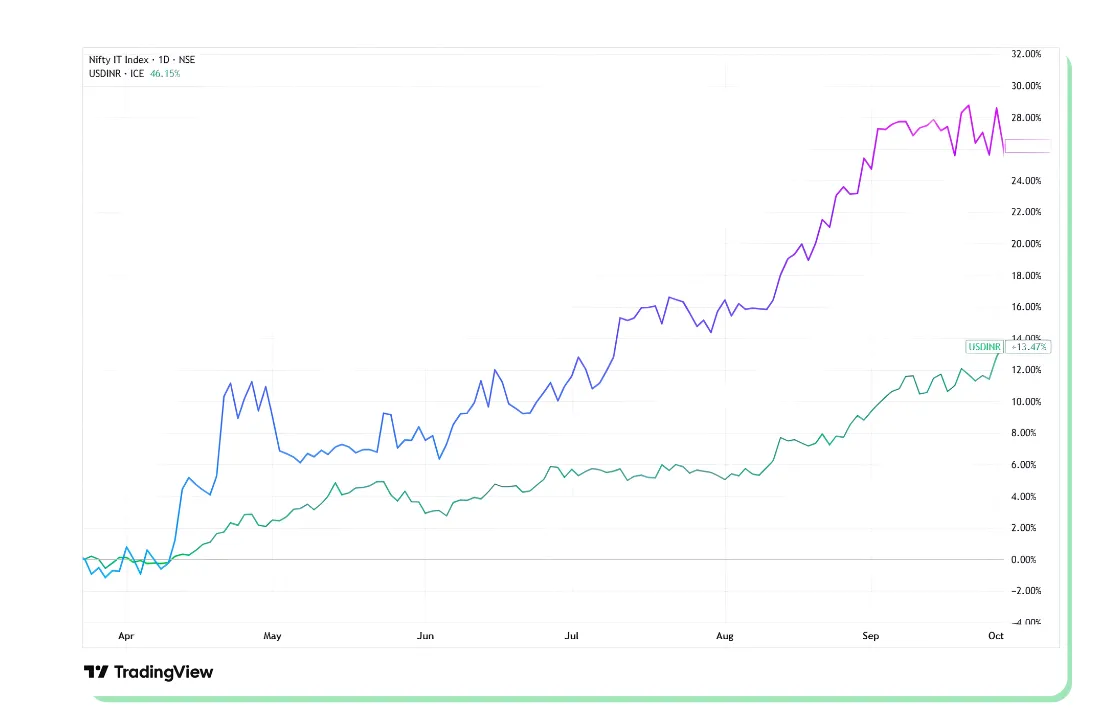

During the calendar year 2018, this relationship held with unusual clarity. Between April and October, the rupee slid from roughly 65 to nearly 74 against the dollar, and over the same stretch Nifty IT surged close to 30 percent. That period strengthened the belief that rupee depreciation and IT stocks often move in the same direction, particularly during phases of strong export growth. Currency translated directly into earnings upgrades across the sector, and the parallel between rupee weakness and stock performance was treated by many market participants as a relatively direct relationship. That prior episode established the mental model that most retail investors carry into the present one.

Also Read: Navigating India's Wastewater Treatment Mega Cycle

How Global Technology Spending Affects Indian IT

At the level of an economy or the global financial system, macroeconomic conditions shape the environment in which companies operate without directly determining what any individual company does within it. For Indian IT, the relevant macro variables extend beyond the rupee to include global technology spending cycles, interest rate environments in developed markets and commodity prices. Spending on IT contracts in the United States and Europe, which together account for the majority of Indian IT revenue, moves with broader GDP growth. When growth slows or uncertainty rises, enterprises defer technology transformation projects or renegotiate existing contracts. This also explains why IT sector US recession risk remains closely monitored by investors, since slower growth in developed markets can delay enterprise technology spending.

In the present period, several macro variables are moving simultaneously and in competing directions. Rupee depreciation of over ten percent in the twelve months preceding May 2026 has created a measurable translation benefit for IT exporters. Against this, Brent crude has climbed to approximately 101.50 dollars per barrel following geopolitical disruptions in the Strait of Hormuz, widening India's import bill and sustaining downward pressure on the currency through a different channel. Global technology spending, meanwhile, remains cautious as enterprises await clarity on how artificial intelligence will reshape their vendor relationships and the structure of large outsourcing contracts.

Micro Fundamentals and Their Relationship to Valuation

Where macroeconomic conditions describe the environment a company operates in, micro fundamentals describe what the company is actually doing within that environment. Revenue guidance, deal pipeline quality, client additions and attrition, margin trajectory and management commentary on near-term demand are all micro signals. Equity valuations reflect not simply the conditions a sector faces but whether its earnings can grow within those conditions.

Of practical significance is that macro tailwinds can be neutralised by micro headwinds of sufficient magnitude. A sector may benefit from a favourable currency for two or three consecutive years while simultaneously experiencing valuation multiple compression due to declining growth visibility. The currency benefit appears in the profit and loss account; the concern about structural demand compression appears in the multiple the market assigns to future earnings. These two forces operate on different timelines and carry different weights at different points in a cycle, which is why reading them together matters more than tracking either in isolation. In practical terms, investors need to track both macro conditions and company-specific execution to analyse IT sector stocks correctly.

What Is AI Deflation in the IT Sector

Through the earnings season of fiscal year 2026, AI-led pricing pressure became an increasingly discussed theme in Indian IT sector analysis. Broadly, it describes a condition in which clients reduce expenditure on traditional IT services as generative artificial intelligence tools lower the cost of tasks that previously required vendor engagement or human labour at scale. The effect on the IT industry is deflationary: the same business outcome is now achieved at lower cost to the client and, correspondingly, at lower revenue for the service provider.

Each of the four largest listed IT companies addressed this dynamic directly in their most recent quarterly results. HCL Technologies CEO C. HCL Technologies management indicated that AI-led efficiency gains could create pricing pressure across certain traditional service lines in the coming fiscal year. TCS management acknowledged a slowdown in growth momentum amid changing client spending patterns. Infosys management highlighted that AI-driven productivity gains could reshape pricing and delivery. Wipro management noted pricing and margin pressures in certain client engagements.Translating these signals into comparable terms is instructive. The issue is particularly relevant for TCS, Infosys, HCL Technologies and Wipro in 2026, as clients increasingly demand productivity-linked pricing models.

Rupee depreciation of approximately ten percent over twelve months can generate a currency-related earnings benefit, depending on hedge positions, pricing structures, and offshore costs. Revenue growth guidance cuts driven by AI deflation, however, are running at 300 to 500 basis points across the sector. The micro headwind exceeds the macro tailwind by a meaningful margin, and equity markets have adjusted valuations accordingly.

Where TCS, Infosys, HCL and Wipro Stand Today

As of early May 2026, all four companies are trading within a narrow range of their respective 52-week lows, as the reference table below indicates.

| Company | Current Price | 52-Week Low | 52-Week High | YTD Decline |

|---|---|---|---|---|

| TCS | 2,379 | 2,346 | 3,630 | 22.8% |

| Infosys | 1,160 | 1,149 | 1,728 | 21.2% |

| HCL Technologies | 1,183 | 1,176 | 1,780 | 26.2% |

| Wipro | 197 | 186 | 273 | 24.4% |

Prices as of May 8, 2026. Source: NSE

The sharp correction across the sector has also pushed several companies close to their IT sector 52 week low levels despite supportive currency trends.

HCL Technologies touched a fresh 52-week low of Rs 1,176 on May 8, closing at Rs 1,183, just 0.19 percent above that level. TCS closed at Rs 2,379, some 1.42 percent above its floor of Rs 2,346. Infosys and Wipro follow a similar pattern, with year-to-date declines of approximately 21 and 24 percent respectively. Taken together, the Nifty IT index has declined 23 percent in 2026, underperforming the Sensex by a considerable margin despite operating in what is, by the standard currency metric, a historically favourable environment.

Also Read: Catching the Tailwind of Indian Shipbuilding Growth

Framework for Analysing Indian IT Sector Stocks

Treating currency as the primary variable in IT sector analysis has historically produced acceptable results when macro conditions were broadly stable and sector growth was intact. Neither condition fully applies at present. A more complete analytical approach requires assessing macro conditions and micro fundamentals together, with explicit attention to which set of factors is carrying more weight in a given cycle.

For macro inputs, the relevant variables in Indian IT are the direction of the rupee against the dollar, the pace of technology spending growth in the United States and Europe, global risk appetite as reflected in FPI flows, and crude oil prices as a proxy for India's external account. Most of these are observable through publicly available data. NSDL publishes daily FPI flow figures, RBI publishes currency and reserve data, and global IT bellwethers such as Accenture signal sector-wide spending trends through their quarterly guidance. Among the most closely watched indicators are IT sector FPI flows, global technology spending guidance, and currency trends.

For micro fundamentals, the central inputs are annual revenue guidance provided by management at the start of each fiscal year, large deal win volumes and their total contract values, headcount changes as a forward-looking indicator of demand, and operating margin direction. These are disclosed through quarterly earnings filings and investor presentations. Reading them systematically alongside macro data produces a more grounded picture of sector dynamics than currency tracking alone. Revenue guidance, operating margin trends, headcount expansion and large deal wins remain critical indicators for evaluating IT sector revenue guidance and future earnings visibility. Even when earnings remain stable, IT sector valuation multiples can compress sharply if markets expect slower long term growth.

Determining which set of factors carries more weight requires assessing relative magnitude rather than simply identifying which direction each is pointing. When macro tailwinds are modest and micro headwinds are structural and broad-based across companies, the latter tend to dominate valuation over the medium term. When sectors face temporary earnings pressure alongside strongly supportive macro conditions, valuation recoveries can outpace the earnings trajectory. In the present period, the Indian IT sector is navigating the former scenario, where a genuine macro tailwind is being outweighed by a structural demand-side shift. Investors also closely monitor the IT sector deal pipeline because large contract wins often provide early signals of future revenue visibility.

Why IT Stocks Fell in 2022 Despite Dollar Strength

From previous cycles, useful precedents exist for the current pattern. During 2022, a sharp appreciation of the dollar against most currencies, including the rupee, initially raised expectations of a strong earnings upgrade cycle for Indian IT. Those upgrades materialised in reported numbers, but stocks declined sharply as investors priced in the risk of a US recession reducing technology budgets. The macro benefit was real; the forward-looking micro concern carried greater weight in market pricing.

Closing

Understanding the difference between a currency tailwind and a structural headwind is essential when analysing valuation cycles in Indian IT. Currency is a necessary input in analysing the Indian IT sector, but it is not a sufficient one. At any point in time, the valuation of an IT company reflects a composite of macroeconomic conditions, structural demand forces and company-level execution. In the current environment, rupee weakness near multi-year lows is providing a measurable, if partial, benefit to earnings. Against this, AI-driven deflation in IT services spending is compressing revenue growth expectations across the sector in a manner that exceeds the currency benefit in magnitude. For long term investors, analysing Indian IT companies now requires balancing currency trends with structural changes in global outsourcing demand and AI-led efficiency shifts. Developing the practice of reading both sets of factors together, and identifying which carries more weight in the current cycle, is the more durable analytical approach for any investor tracking this sector.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.