Think of Samhi Hotels Ltd like a master house-flipper, but for hotels. Imagine someone who has a talent for finding rundown, badly-managed houses in great locations. They buy them cheap, renovate them, put up a well-known brand name on the door, and the property suddenly starts earning far more money. They keep the property, collect the income for decades, and repeat the process with more properties. That is exactly what Samhi Hotels does, except with hotels in India's biggest office cities.

The Samhi Hotels Turnaround: Five Pillars of the Business

They find neglected hotels in great locations and buy below replacement cost

Samhi buys hotels that are poorly run, barely half-full, and priced cheaply because sellers are distressed. Average cost: ₹70 lakh per room vs ₹200-300 lakh to build one fresh.

They renovate and hand them to big global brands

Samhi spends ₹10-20 lakh per room on renovations like new rooms, modern bathrooms, upgraded F&B. Total cost is still well below replacement value. Marriott International, Hyatt Hotels Corporation, or InterContinental Hotels Group takes over operations. Suddenly the hotel is in Marriott's booking system reaching 200 million loyalty members worldwide. Occupancy jumps from 35-40% to 70-75% within 12-18 months. A poorly-run mid-scale hotel charging ₹2,000/night under an unknown brand can charge ₹5,000-8,000/night under Fairfield by Marriott. The room is the same. The brand changes everything.

Samhi keeps 95% of the money; brands take 5% as fee

Samhi owns the hotel and gets all the revenue. It just pays the brand operator about 4-5% of revenue as a management fee. Samhi controls the finances; the brand controls the daily running.

They are present only where businesses are growing fastest

Bangalore, Hyderabad, Pune, Delhi NCR — cities where offices are expanding and corporate travellers fill hotels every weekday. No leisure-dependent resorts. No uncertain markets.

Interest costs are collapsing, turning losses into profits

Samhi carried ₹2,940 Cr of debt before its IPO. That has now fallen to ₹1,450 Cr. Interest cost dropped from ₹522 Cr/year (FY23) to ~₹200 Cr (FY26E). This single change is transforming the P&L.

The Samhi Hotels Business Model: Freehold and Leasehold Ownership

Understanding Samhi Hotels freehold and leasehold structures is essential to evaluating returns, as the two models differ meaningfully in capital intensity and ROCE Samhi follows two distinct ownership models for its hotel portfolio, which is an important factor in evaluating the company. Under the freehold model, which contributes around 87% of revenue, Samhi owns both the land and the building outright and does not incur any lease payments. The capital required is approximately ₹70–80 lakh per room, including land, construction, and fit-out, and this model typically generates a return on capital (ROCE) of around 11%. Key examples include properties such as Sheraton Hyderabad Hotel and Fairfield by Marriott Bengaluru Outer Ring Road. One of the advantages of this structure is that ownership of real estate provides an asset-backed downside protection in weaker cycles.

Think of it like owning a McDonald's building but having McDonald's run the restaurant. You own the property and collect most of the profits. McDonald's puts its name on the door, trains the staff, and handles the menu and charges you a small fee for doing so. Samhi is the building owner. Marriott is the McDonald's corporate team. The customers see Marriott; the money flows to Samhi.

Samhi now earns ₹200-450 Cr of revenue from each acquired hotel per year, indefinitely. The real estate appreciates in value. The hotel runs itself via the brand operator.

The Sheraton Hyderabad Hotel serves as a strong example of SAMHI’s value creation strategy. The property was acquired in 2013 for approximately ₹170 Cr, comprising 272 rooms, and was subsequently fully renovated and rebranded under the Sheraton by Marriott International. Prior to acquisition, the hotel generated a RevPAR (revenue per room per night) of around ₹1,400, which has since increased to approximately ₹8,100, representing a 5.8x improvement. The property now generates annual revenue of about ₹97 Cr, translating into a 57% annual return on the original investment, sustained over time.

At the same time, Samhi is increasingly shifting towards a leasehold model, as it allows the company to achieve similar profitability with significantly lower capital investment. This shift improves capital efficiency, with ROCE increasing from around 11% in the freehold model to approximately 18% in leasehold structures. Notably, one of the best-performing assets in its portfolio, Holiday Inn Express Hyderabad HITEC City, operates under a leasehold model and delivers an exceptional return on capital of around 45% annually, highlighting the scalability and efficiency of this approach.

Why Is This a Good Time to Be in Indian Hotels?

The India hospitality sector is experiencing one of its strongest demand cycles in over a decade, making this an important backdrop for evaluating Samhi Hotels.

India Hotel Supply and Demand: The Structural Tailwind Driving Samhi

The India hotel industry is in its longest sustained upcycle in recent memory, with demand growing at 8–10% annually against supply additions of just 2–5%. Hotels make more money when more guests want rooms than there are rooms available. Right now, India's branded hotels are in exactly that situation, and it has lasted for 3+ years with no end in sight. India branded hotels are the primary beneficiaries of this demand-supply gap, as travellers increasingly prefer globally recognized chains over independent properties.

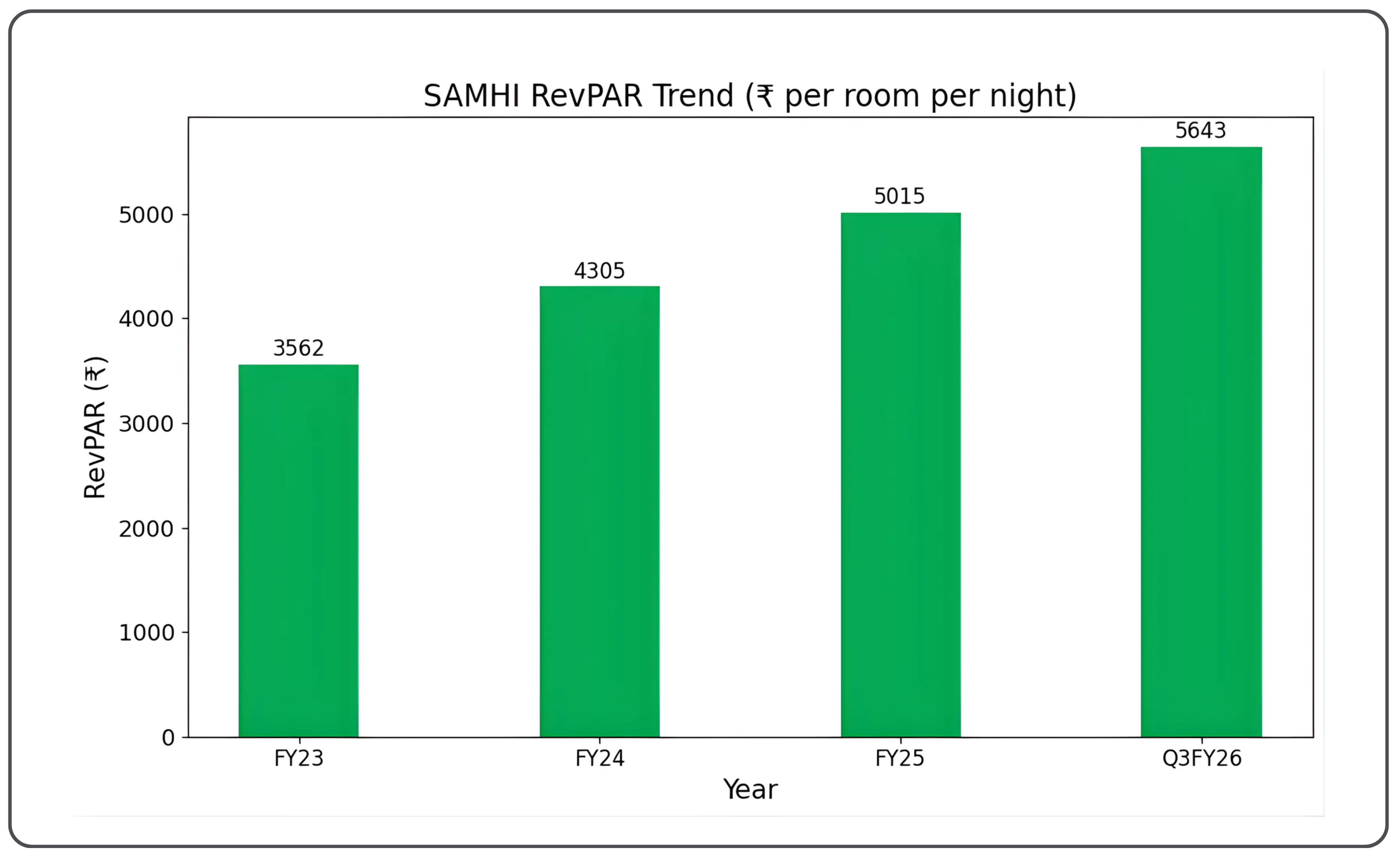

Samhi Hotels RevPAR: Four Years of Sustained Growth

What does this gap mean in practice? Hotels can charge more per room and still stay fuller. That is exactly what RevPAR (Revenue Per Available Room: the key hotel performance metric) measures:

| Year | Revenue per Room per Night (RevPAR — Same hotel) |

|---|---|

| FY23 | ₹3,562 per room per night |

| FY24 | ₹4,305 per room per night (+20.9% in one year) |

| FY25 | ₹5,015 per room per night (+16.5%) |

| Q3FY26 (latest) | ₹5,643 per room per night (+13.3%) |

The trend has been sustained for 4 consecutive years. The reason is structural:

India added 22.5 million sq ft of office space in a single quarter (Q2FY24). Every new office employee is a potential hotel guest.

Air passenger traffic: 295 million passengers in FY25, growing 8.7% annually. More travellers need more hotel rooms.

Foreign tourist arrivals are still below 2019 levels, meaning further upside as they recover.

New hotel construction takes 4-5 years. The demand Samhi is capturing today has barely any new supply competing against it.

Samhi’s key markets are the strongest markets in the country. Nearly 75% of all new hotel supply in India is being added in Tier-2 and Tier-3 cities, while Samhi operates exclusively in Tier-1 cities such as Bangalore, Hyderabad, Pune, and Delhi NCR. In these markets, demand is growing at around 9%, whereas net new supply increased by just 0.6% in Q1FY25. As a result, national supply data significantly understates how tight and supply-constrained Samhi’s actual operating markets are.

The same structural tailwind dynamic playing out in Indian hotels is examined from a different angle in Evaluating India's Cement Industry Amid Structural Tailwinds, where supply constraints and demand growth converge to create a compelling sectoral opportunity.

Why Bangalore and Hyderabad Matter So Much

Two cities account for over 55% of Samhi's revenue. Understanding them is understanding Samhi.

| City | Why it matters for Samhi |

|---|---|

| Bangalore | World's largest office leasing market in CY2024 — 14 million sq ft absorbed. More offices = more business travellers = more hotel guests every night. |

| Hyderabad | Home to Google's second-largest office globally, Amazon, Microsoft, Nvidia, Accenture. Hotel supply growth is minimal despite explosive tech-sector growth. |

| Pune | Pharma + IT corridor. Hyatt Regency is Samhi's best-performing upscale asset here. |

| Delhi NCR | Government + corporate hub. Growing at 10% RevPAR annually. |

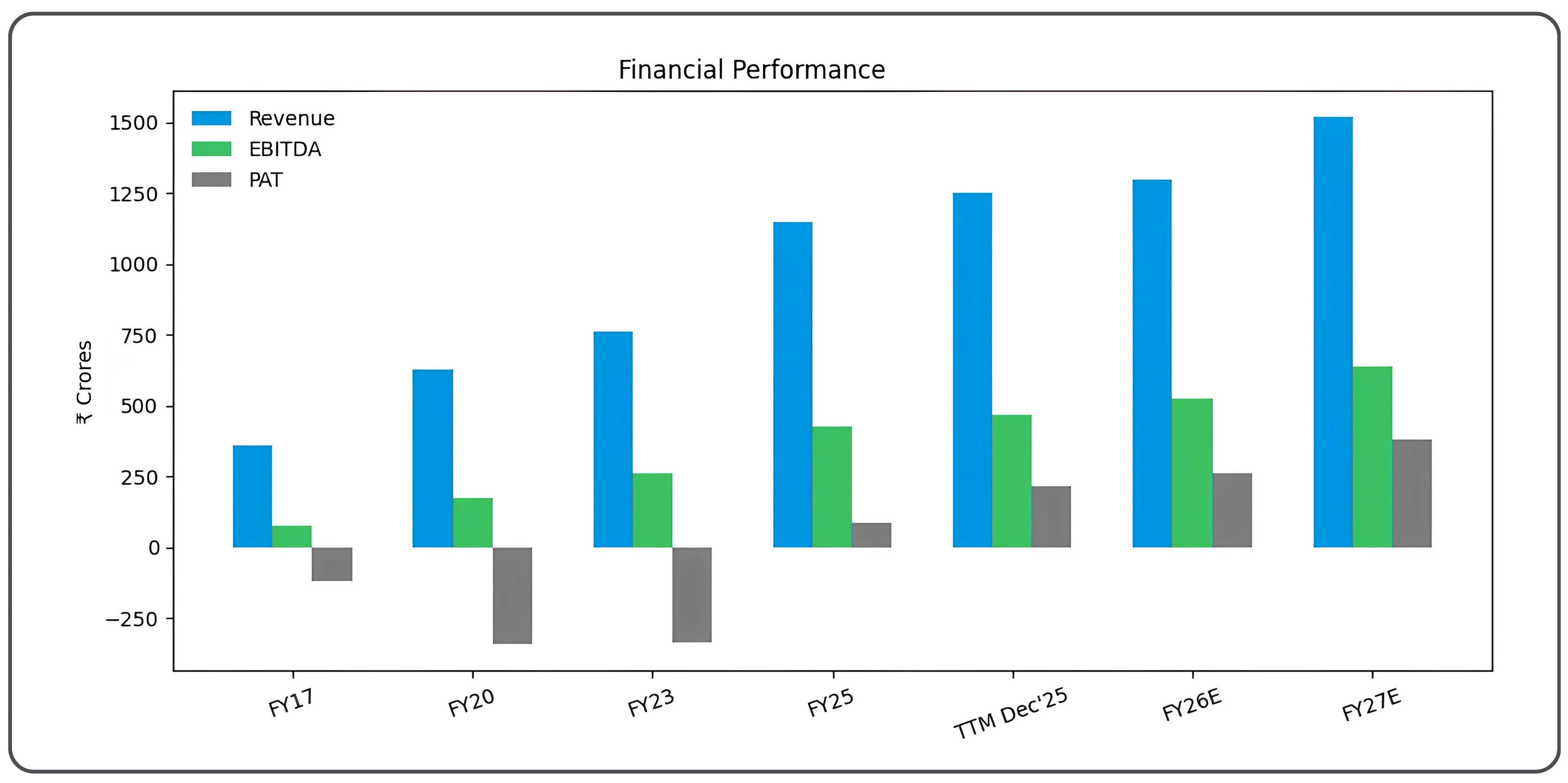

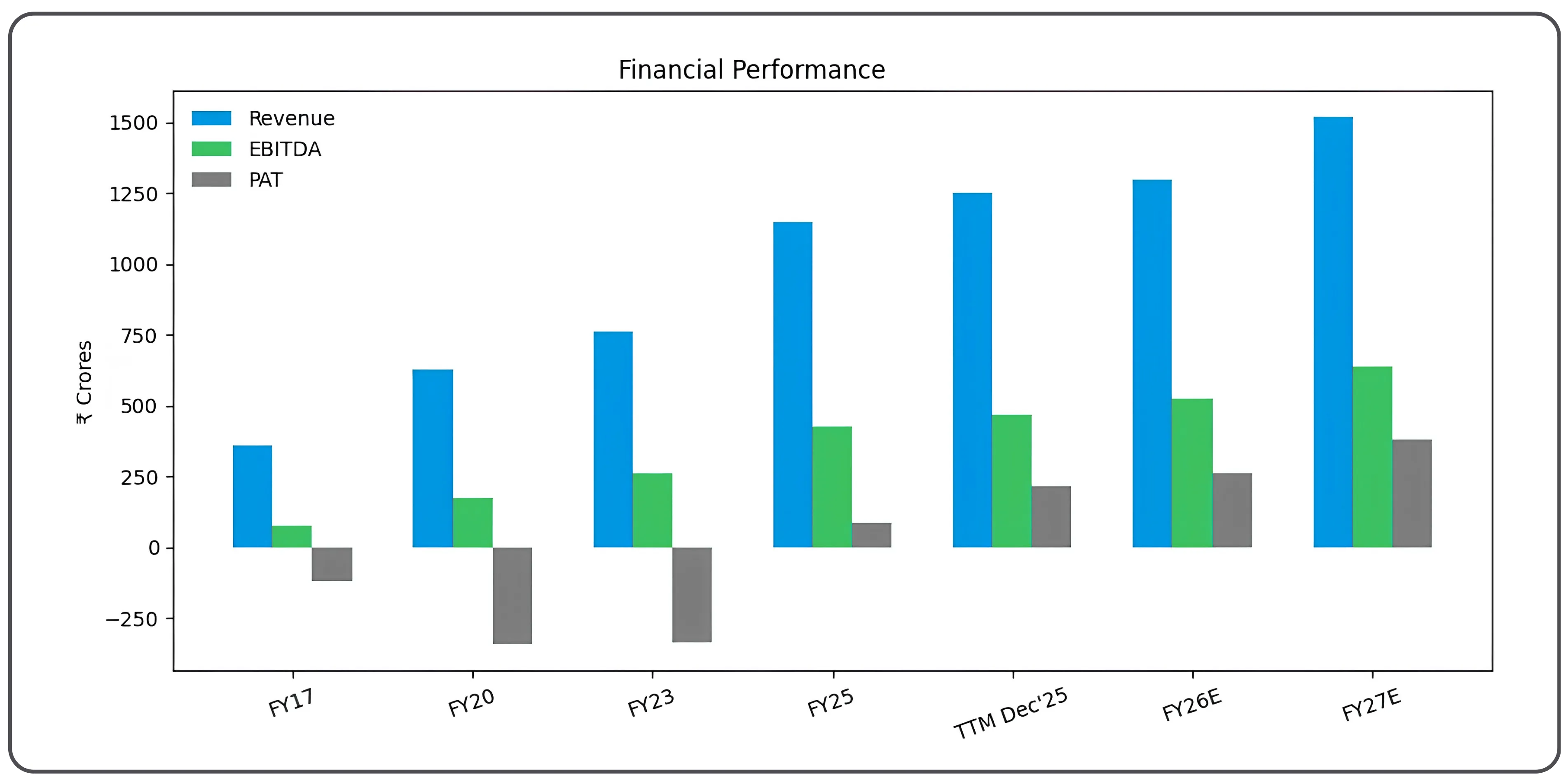

The Financial Story of Samhi Hotels

| FY17 | FY20 | FY23 | FY25 | TTM Dec'25 | FY26E | FY27E | |

|---|---|---|---|---|---|---|---|

| Hotels / Rooms | 8 / 1,460 | 27 / 4,050 | 25 / 3,839 | 32 / 4,948 | 31 / 4,904 | – | – |

| Revenue | 357.2 | 627.6 | 761.4 | 1,149.7 | 1,249.1 | ~₹1,296 Cr +13% YoY (forecast) |

₹1,516.7 Cr +17% YoY (forecast) |

| EBITDA | 74.8 | 172.0 | 260.6 | 425.7 | 468.6 | ₹524 Cr (40.5% margin) | ₹637 Cr (42% margin) |

| PBT | (145.1) | (206.3) | (357.7) | 80.1 | 162.3 | – | – |

| PAT | (118.7) | (344.0) | (338.6) | 85.5 | 213.0 | ₹260 Cr (forecast) | ₹380 Cr (forecast) |

Samhi's profitability trajectory shows a clear turnaround over recent years. The company reported deep losses of ₹478 Cr in FY21 during the COVID period, followed by a loss of ₹443 Cr in FY22. Losses began to narrow in FY23 to ₹339 Cr and further improved to ₹235 Cr in FY24, indicating steady operational recovery. In FY25, Samhi reported a profit of ₹86 Cr, marking its first annual profit in 15 years. This momentum is expected to accelerate, with profits projected to rise to around ₹260 Cr in FY26 and further to approximately ₹380 Cr in FY27, reflecting strong and sustained growth. Samhi Hotels EBITDA has grown from ₹260 Cr in FY23 to ₹468 Cr on a trailing twelve-month basis, with margins expanding toward 40% as interest costs decline.

A 40% EBITDA margin means that for every ₹100 of hotel revenue, ₹40 is operating profit before interest and taxes. For comparison, Indian Hotels Company Limited operates at around a 34% margin, while most manufacturing companies typically generate margins in the 10–15% range. Hotels with strong brands in supply-constrained cities can achieve these elevated margins once they are fully operational and stabilized.

This is the number that has been destroying Samhi's profits for years, and is now the biggest driver of its recovery. Samhi borrowed heavily to build its portfolio. Those loans charged very high interest:

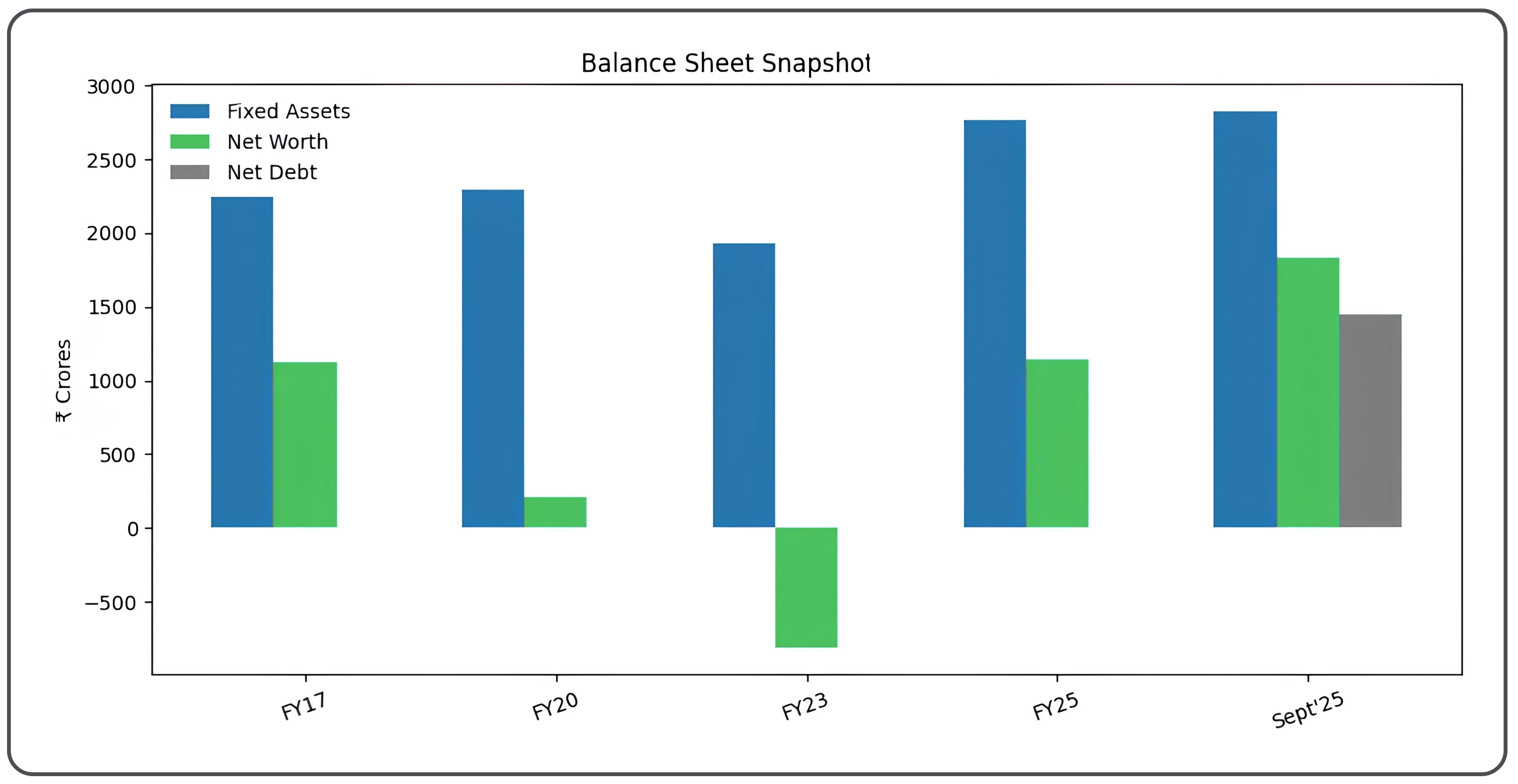

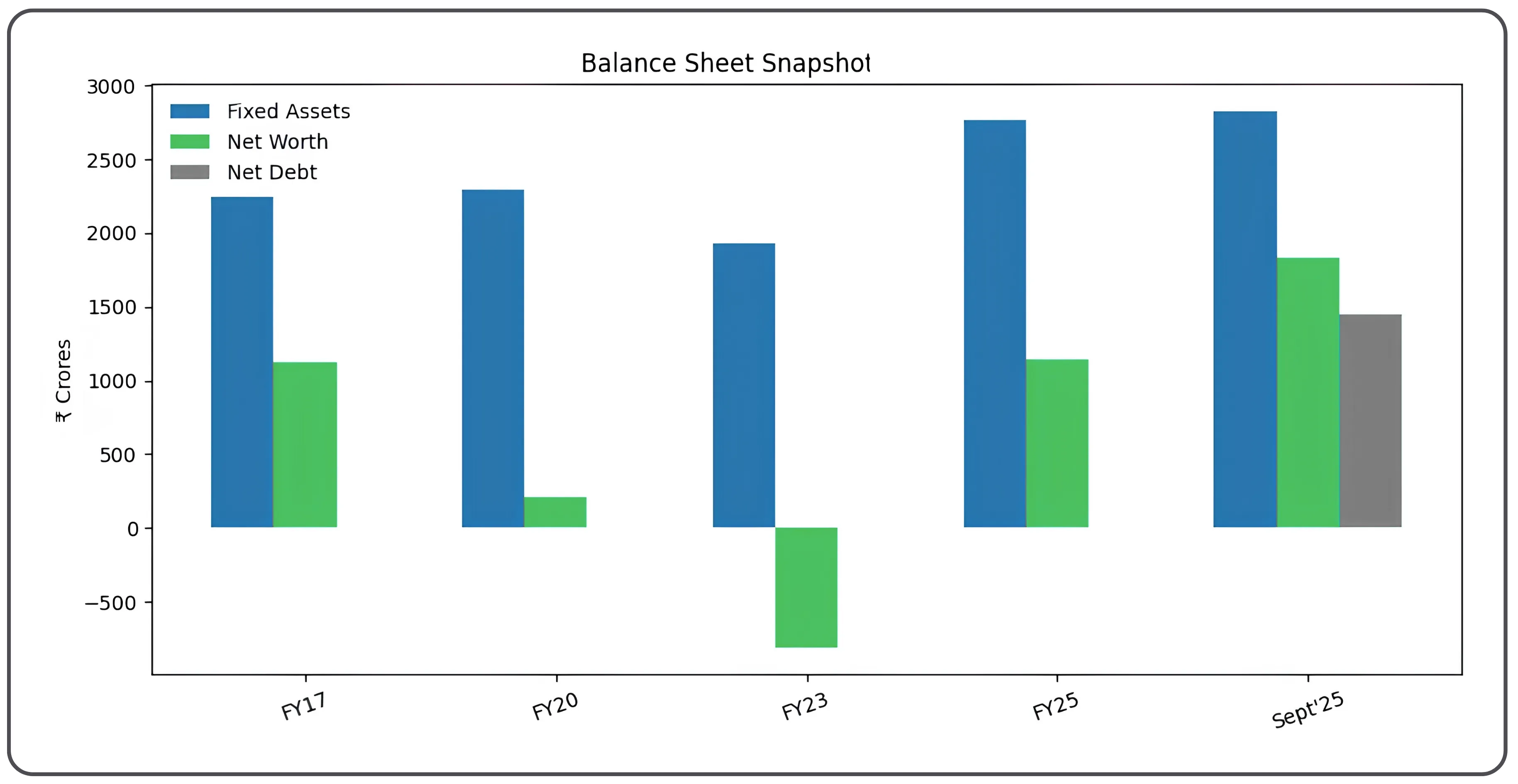

Table 2: Balance Sheet Snapshot (₹ Crore)

| FY17 | FY20 | FY23 | FY25 | Sept'25 | |

|---|---|---|---|---|---|

| Fixed Assets | 2,243.5 | 2,297.0 | 1,929.1 | 2,765.7 | 2,826.4 |

| Net Worth | 1,127.3 | 211.9 | (807.6) | 1,142.1 | 1,834.2 |

| Net Debt | — | — | — | — | 1,450.3 |

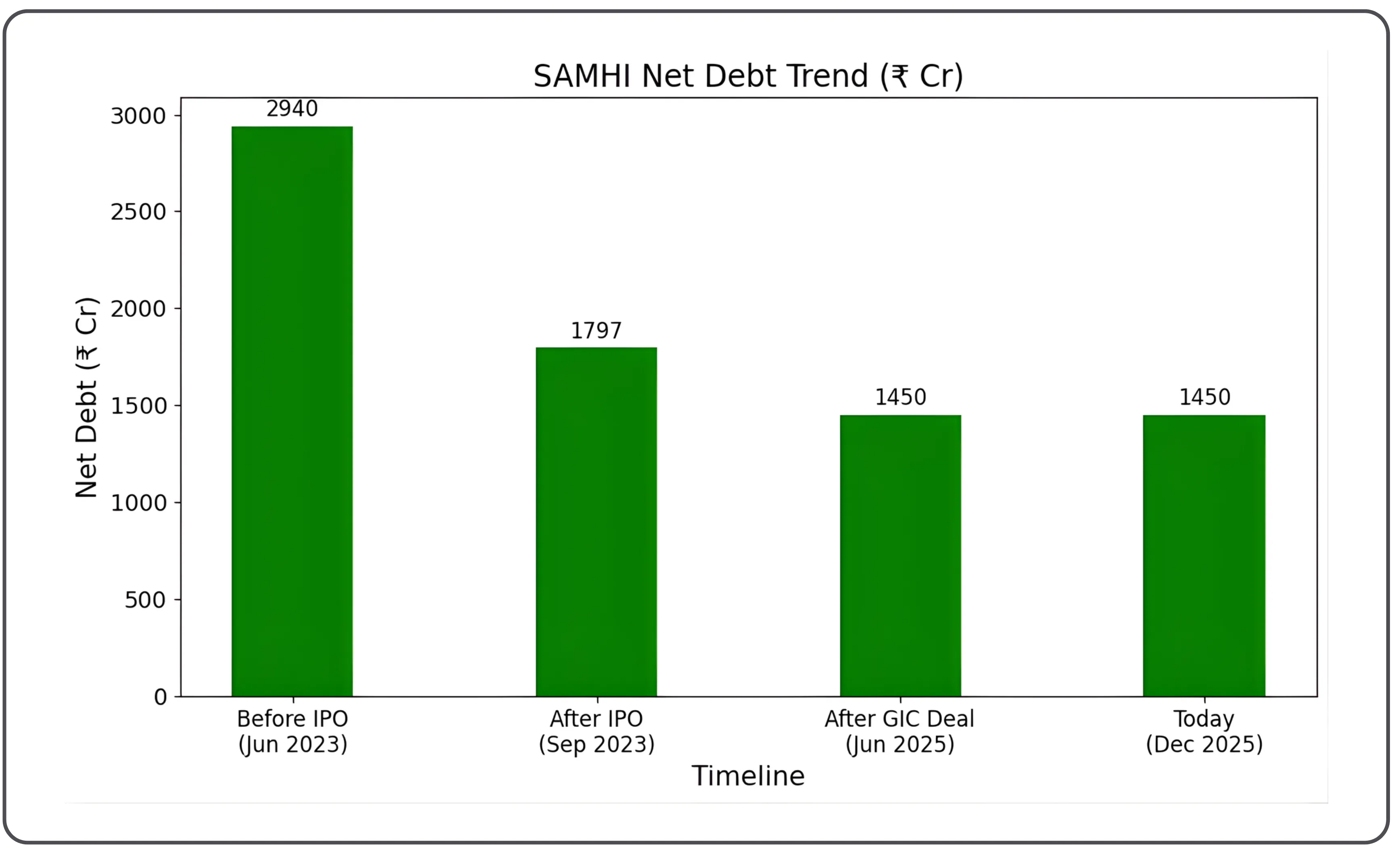

Samhi Hotels Debt Reduction: From ₹2,940 Cr to ₹1,450 Cr

| Period | Interest Paid to Banks (Annual) |

|---|---|

| FY22 Annual Interest Cost | ₹562 Cr — eating up ALL operating profit and more |

| FY23 Annual Interest Cost | ₹451 Cr — still enormous |

| FY24 Annual Interest Cost | ₹345 Cr — falling after IPO debt repayment |

| FY25 Annual Interest Cost | ₹229 Cr — big drop |

| FY26E Annual Interest Cost | ~₹135 Cr — after GIC deal paid off ₹600 Cr of debt |

| FY27E Annual Interest Cost | ~₹120 Cr — still falling |

Since the Samhi Hotels IPO in late 2023, the company has used proceeds to cut net debt from ₹2,940 Cr to ₹1,450 Cr.

Debt — Where Things Stand Today

| Details | |

|---|---|

| Before IPO (June 2023) | ₹2,940 Cr net debt — very high, interest rate 13% |

| After IPO (Sep 2023) | ₹1,797 Cr — used IPO proceeds to repay |

| After GIC deal (Jun 2025) | ₹1,450 Cr — GIC paid ₹750 Cr for 35% stake in 3 hotels |

| Today (Dec 2025) | ₹1,450 Cr — holding steady at this level |

| Interest rate on debt | 8.5% — down from 13%. Latest new loan at 7.55%! |

| Target by FY28 | ₹1,200 Cr or less (2.5x EBITDA) |

The Samhi Hotels GIC deal, concluded in June 2025, saw GIC pay ₹750 Cr for a 35% stake in three hotels, allowing Samhi to retire ₹600 Cr of high-cost debt without shareholder dilution.

What Gives Samhi Its Edge?

Samhi's approach mirrors the hotel franchise model in India, where the owner bears capital costs while the brand operator drives occupancy through its loyalty system and distribution network.

Buying cheap — below replacement cost

Samhi paid an average of ₹70 lakh per room over 13 years. Today it would cost ₹150-300 lakh to build the same room fresh. This gap is permanent and it can never be replicated because those historical deals are done. It creates a cost advantage that drives superior returns forever.

Samhi Hotels and Marriott: India's Largest Branded Hotel Partnership

Samhi is one of the largest owners of Marriott India hotels, holding 40% of all Fairfield by Marriott rooms and significant stakes in Sheraton, Courtyard, and W by Marriott properties. This gives it bargaining power with Marriott International that individual hotel owners can never have. Marriott NEEDS Samhi's portfolio to perform well.

In addition to its Marriott partnership, Samhi Hotels and Hyatt work together on upscale properties, with the Hyatt Regency Pune serving as one of its best-performing assets. Samhi Hotels and IHG together operate 10 Holiday Inn Express properties across India, with Samhi owning 70% of all IHG-branded rooms in this category.

Samhi Intel — data advantage

Samhi built a proprietary daily data tracking system it calls Samhi Intel. It monitors occupancy, pricing, and competitive supply every single day across all 32 hotels. Individual hotel owners guess. Samhi knows exactly what rates to charge, when to discount, and when to hold pricing firm.

Only 30 corporate employees

All hotel operations are outsourced to Marriott International/Hyatt Hotels Corporation/InterContinental Hotels Group. Samhi itself has just 30 permanent staff. This makes the company extremely lean with negligible fixed overheads. Every rupee of additional revenue flows almost entirely to profit.

13 years of deal-making experience

Knowing which hotels to buy, at what price, in which micro-market, requires deep expertise that takes years to develop. Samhi's team has averaged 14+ years at the company. No competitor has this institutional knowledge of Indian hotel deal-making.

The 'Sheraton Effect' — Why Rebranding is So Powerful

India business hotels in Tier-1 cities are experiencing near-peak occupancies as corporate travel rebounds and office absorption hits record levels. The single best proof of Samhi's competitive advantage is what happens to a hotel's performance after Samhi buys it and rebrands it. Here are three real examples from their portfolio:

| Property | RevPAR Before | RevPAR After | Improvement | How it happened |

|---|---|---|---|---|

| Sheraton Hyderabad | ₹1,400/night | ₹8,100/night | 5.8x (480% higher) | Bought in 2013. Full renovation. Rebranded Sheraton by Marriott. Business travellers now pay premium. |

| Holiday Inn Express (10 hotels) | ₹1,100/night | ₹2,800/night | 2.5x (155% higher) | Bought as various small hotels. Renovated. Rebranded. IHG loyalty system brought consistent bookings. |

| Fairfield Bangalore City Centre | ₹1,279/night | ₹4,369/night | 3.4x (241% higher) | Originally a 45% occupied property. Now 76% occupancy at 3x the room rate. |

India hotel RevPAR growth has averaged above 15% for three consecutive years, with Samhi's same-store portfolio tracking the national trend closely. Samhi Hotels Bangalore properties include Fairfield by Marriott on the Outer Ring Road and the upcoming Tribute Portfolio and Westin in Whitefield, Bangalore's fastest-growing IT corridor. Samhi Hotels Hyderabad assets include the Sheraton Hyderabad Hotel and the upcoming W Hotel in HITEC City, anchoring the company's presence in one of India's most active tech markets.

Where Is Growth Coming From?

Samhi's current 32 hotels are just the beginning. The company has a clear, committed pipeline of new rooms opening over the next 5 years. Here is what is coming and why it matters.

The Samhi Hotels pipeline includes 11 committed projects adding over 1,900 rooms between FY26 and FY30, representing a significant step-up in revenue capacity

The Near-Term Pipeline (FY26–FY27)

W Hotel, HITEC City Hyderabad — 170 rooms

W Hotel, HITEC City Hyderabad — 170 rooms Scheduled for FY27, this project involves converting an empty office building into a premium W by Marriott, making it Samhi’s most upscale hotel yet. The property is expected to generate revenue of around ₹150 Cr per year at maturity.

Courtyard by Marriott, Pune — 217 rooms

Planned for FY27, this involves rebranding an existing Four Points property into Courtyard by Marriott International. The building remains the same, but the brand upgrade is expected to drive an immediate increase in average room rates.

Fairfield by Marriott, Delhi — 142 rooms

Targeted for FY27, this project includes rebranding the Caspia Delhi property into Fairfield by Marriott International. The Marriott contract has already been signed, providing visibility on execution.

HIEX Whitefield, Bangalore — 56 new rooms

Expected in FY26, this expansion adds new rooms to an existing Holiday Inn Express property. It represents pure incremental revenue with no additional property acquisition cost.

Sheraton Hyderabad — 42 new rooms

Scheduled for FY26, this involves converting underutilized F&B space into hotel rooms. With zero land cost involved, this project is expected to deliver one of the highest returns on investment.

The Big-Ticket Projects (FY28–FY30)

Tribute Portfolio + Westin, Whitefield Bangalore — 377 rooms

This project is expected to generate around ₹230 Cr per year. It involves the Trinity hotel (bought for ₹205 Cr in Oct-24) along with a 200+ room expansion. It is located in Bangalore's fastest-growing IT corridor, making it a high-demand micro-market.

Samhi Hotels Navi Mumbai: The 700-Room Airport Project

This development is expected to generate approximately ₹325 Cr per year. It is located near the upcoming Navi Mumbai International Airport, which is planned to handle 110 million passengers annually. The land was acquired at near-zero cost through the ACIC deal. This single project accounts for nearly 28% of Samhi’s current total revenue. The Navi Mumbai opportunity is a significant value driver for Samhi. The land for this project was acquired for just ₹26 Cr as part of the ACIC portfolio deal and was previously written off as worthless during MIDC disputes before being fully reinstated in Q2FY26. Samhi now plans to develop a 700-room dual-branded hotel comprising Westin and Fairfield by Marriott International, located near India’s newest and largest airport. At maturity, this single project is expected to generate around ₹325 Cr in revenue and ₹180 Cr in EBITDA, which is equivalent to nearly 40% of Samhi’s entire FY25 profits. Notably, the effective land cost for this project is close to zero, making it an exceptionally high-return opportunity.

One Financial District, Hyderabad — 260 rooms

This project is expected to generate around ₹70 Cr per year. It is a mid-scale hotel located within Hyderabad’s most premium office complex, operating under a variable lease model with near-zero land cost.

Samhi Hotels and RARE India: A New Chapter in Experiential Travel

In March 2026, Samhi made a surprising move: it acquired 70% of RARE India — a 20-year-old platform of 67 heritage hotels, wildlife lodges, and eco-retreats across India, Nepal, and Bhutan.

RARE India is a curated portfolio of 67 boutique heritage and experiential hotels, including forts, palaces, and nature lodges located in unique destinations. These are not mainstream business hotels but part of India’s oldest curated experiential travel platform.

Samhi acquired a 70% stake in RARE India for ₹47 Cr, which represents just 1.6% of its market capitalization and is therefore financially immaterial at the current scale.

The strategic rationale lies in integrating RARE India with Marriott International through the ‘Outdoor Collection by Marriott Bonvoy’, marking India’s first such initiative. This move brings 67 heritage hotels into Marriott’s 210-million-member global loyalty ecosystem, significantly enhancing visibility and demand potential.

If the strategy executes well, the platform has the potential to generate ₹90–100 Cr in revenue over the next 3–4 years, particularly if the network expands to 120–150 hotels.

However, there are execution risks. Heritage hotel owners may resist adopting Marriott’s standardized processes, and transitioning from a subscription-based model to a consumer-facing platform could take time. This remains an early-stage initiative rather than a guaranteed outcome.

Overall, the investment represents a ₹47 Cr option with meaningful upside potential. Even in a downside scenario where the initiative does not succeed, the financial impact is limited to less than 2% of Samhi’s market cap. If successful, it can create a new ₹100 Cr revenue stream for the company.

What Can Go Wrong? — Samhi Hotels Risk Assessment

India’s economic slowdown is a major risk for Samhi. If GDP growth declines from around 7% to 3–4%, corporate travel budgets tend to shrink, leading to lower occupancy and reduced room rates. This could result in a 15–20% drop in Samhi’s revenue. Such scenarios have played out before, with revenue falling nearly 70% during COVID and around 15% during the 2008–09 period. However, the company is better positioned today, with debt reduced to ₹1,450 Cr from ₹2,940 Cr prior to its IPO, which improves its ability to withstand a moderate downturn.

Changes in GST regulations present a medium-level risk. In late 2025, the government removed input tax credit on hotel rooms priced below ₹7,500 per night, effectively increasing costs by 150–200 basis points for Samhi’s mid-scale portfolio. The company is attempting to pass on this impact through price increases. Early indications from Q3FY26, where mid-scale revenue grew by 16%, suggest some success, although the full impact is yet to be confirmed.

Another medium risk relates to debt levels. Samhi is expected to require over ₹1,000 Cr to develop the Navi Mumbai project between FY27 and FY30. If internal cash flows are insufficient and the company takes on additional borrowing, the benefits from reduced interest costs could reverse. A quarterly debt level exceeding ₹2,000 Cr would serve as an early warning signal.

An increase in hotel supply in key markets such as Bangalore and Hyderabad is also a medium risk. A surge in new developments could intensify competition and weaken pricing power. At present, supply growth in Tier-1 cities remains limited at around 0.6–2% annually, but any significant rise in approvals, particularly in micro-markets like Outer Ring Road or HITEC City, should be monitored closely.

Execution delays in the project pipeline remain another medium concern. Of the 11 committed projects, six have already been delayed by one to four quarters. While such delays typically push out revenue timelines rather than eliminate them, management’s optimistic timelines suggest investors should factor in an additional two to three quarters for project completion.

Finally, the RARE India integration represents a low-risk factor, with only ₹47 Cr at stake. This initiative is a strategic bet on India’s experiential travel segment, but there are execution challenges, including potential resistance from heritage hotel owners to standardized systems and the time required to transition to a consumer-facing model. Given Samhi’s market capitalization of around ₹2,950 Cr, even a complete write-off would have a negligible financial impact.

The Stress Test — What Happens in a Bad Scenario?

Occupancy falls 10%, room rates fall 8%, interest rates rise 1%

Under these assumptions (serious but not catastrophic) Samhi's FY27 EBITDA falls from ₹637 Cr to approximately ₹421 Cr. Net Debt/EBITDA rises from 2.8x to around 3.9x, still well below the 5.5–6x threshold at which debt covenants would be breached. The company would remain solvent, continue operating, and would not need to raise emergency equity. This is precisely what distinguishes Samhi in 2026 from Samhi in 2023, a balance sheet that has halved its debt from ₹2,940 Cr to ₹1,450 Cr can now absorb a serious downturn without existential risk.

The one risk that really matters

A deep, sustained India-specific recession, GDP below 4% for two or more consecutive years, coinciding with Samhi needing to borrow ₹800–1,000 Cr for its Navi Mumbai expansion would be the most damaging combination. Debt rising while EBITDA contracts could push Net Debt/EBITDA back toward 5x. This scenario is unlikely, but it is the one that would make this investment genuinely painful. Critically, it requires two things to go wrong simultaneously, a macro shock and a poor capital allocation decision by management. Neither alone would be fatal.

Samhi Hotels Valuation: Three Methods and What Each Reveals

At the current Samhi Hotels share price of ₹134 (as of April 1, 2026), the stock trades at just 0.35x its net asset value.

Method 1: Samhi Hotels EV/EBITDA: Cycle-Trough Pricing on a Growing Business

Enterprise Value (EV) = what you pay for the entire company including its debt. EBITDA = annual operating profit. EV/EBITDA tells you how many years of operating profit you are paying for the business.

What does 6.9x EV/EBITDA mean?

Imagine a shop earns ₹100 of operating profit every year. At 6.9x, you buy the entire shop (including its loans) for ₹690. At 14x (where Taj Hotels trades), you would pay ₹1,400 for that same shop. Samhi is priced as if it will barely grow, yet its same-store revenue grew 13% last quarter. The gap between what the market is pricing and what the business is doing is enormous.

6.9x FY27 EBITDA is cycle-trough pricing for a company at its earnings peak: Hotels historically trade at 6-8x EV/EBITDA only during deep recessions when profits are falling. Samhi's profits are GROWING at 20%+ per year. At 6.9x, you are getting a growing business at a distressed price.

Method 2: Net Asset Value — What Are the Hotels Actually Worth?

Hotels are real estate. They can be valued on their underlying asset value, independent of earnings. This gives you a floor price, what you would get if everything was sold off.

| Asset Component | Estimated Value |

|---|---|

| 1,074 upscale/upper upscale rooms @ ₹4 Cr/key | ₹4,296 Cr |

| 2,163 upper mid-scale rooms @ ₹1.5 Cr/key | ₹3,245 Cr |

| 1,564 mid-scale rooms @ ₹0.7 Cr/key (leasehold) | ₹1,095 Cr |

| Pipeline rooms (1,900 at CWIP cost) | ₹1,900 Cr |

| Gross Asset Value | ₹10,536 Cr |

| Less: Net Debt | (₹1,450 Cr) |

| Less: GIC Minority Interest (35% in 3 hotels) | (~₹600 Cr) |

| Net Asset Value (NAV) for Samhi shareholders | ₹8,486 Cr = ₹387/share |

| Current share price | ₹134 = 0.35x NAV |

At the current market price of ₹134, you are buying ₹1 of real estate and hotel assets for just ₹0.35 paise. Indian Hotels (Taj) trades at 3-4x its asset value. Samhi trades at one-third of its asset value.

Samhi Hotels NAV stands at approximately ₹387 per share based on per-key valuations of its existing portfolio, implying the stock trades at just 35 paise on the rupee.

Method 3: Per-Room Market Cap — The Simplest Check

| Company | Market Cap per Hotel Room |

|---|---|

| Samhi @ ₹134 | ₹0.60 Cr per room — LOWEST IN THE SECTOR |

| Lemon Tree Hotels (lower quality) | ₹0.75 Cr per room — trades at PREMIUM to Samhi |

| Chalet Hotels | ₹3.75 Cr per room |

| Indian Hotels (Taj) | ₹15+ Cr per owned room |

Lemon Tree operates lower-quality mid-scale rooms, has higher debt (3.5x ND/EBITDA vs Samhi's 3.0x), and lower EBITDA margins (32% vs 38.6%). Despite inferior metrics on every measure, Lemon Tree trades at a 25% PREMIUM to Samhi on a per-room basis. This divergence is hard to justify on fundamentals. On a Samhi Hotels per room basis, the stock values each key at just ₹0.60 Cr, a discount to every comparable peer including lower-quality operators like Lemon Tree.

The same valuation gap dynamic is explored in depth in Analysing ITC Limited's Deep Value and Structural Growth, where a fundamentally strong business traded at a discount for years before the market recognised its true worth.

The Three Scenarios

| Scenario | What Needs to Happen | FY27E EBITDA (₹ Cr) | FY27E PAT (₹ Cr) | FY27E EPS (₹) | P/E at CMP |

|---|---|---|---|---|---|

| Bull | Pipeline opens on time. GST passed through. Re-rating to peers. | 700 | 326 | 14.8 | 9.1x |

| Base | 9% RevPAR growth. 6-month delays. Gradual de-rating. | 637 | 279 | 12.7 | 10.6x |

| Mild Bear | GST unresolved. Cycle slows to 4% GDP growth. | 520 | 191 | 8.7 | 15.4x |

| Deep Bear | Recession + debt spiral. Cycle turns. | 380 | 86 | 3.9 | 34.4x |

P/E at CMP = ₹134 as on April 1, 2026. Industry PE: 25x. Current stock P/E: 19.2x.

Where the Business Stands Today

Samhi Hotels is not a typical hotel company; it is a capital allocation machine that spent 13 years quietly assembling a portfolio of undervalued real estate in India's most supply-constrained business cities, then used brand partnerships with Marriott, Hyatt, and IHG to unlock that value. The hard part is already done. The debt that buried its profits for over a decade has been halved, interest costs are approaching levels where earnings can compound freely, and the same-store business is growing at 13% RevPAR even before the pipeline hotels contribute a single rupee. At ₹134, the market is pricing Samhi as if it were a distressed company in a deteriorating cycle, yet the balance sheet is the strongest it has been since inception, occupancies are near peak, and a 700-room Navi Mumbai project sits on land that effectively cost nothing. The valuation disconnect across every methodology (EV/EBITDA, NAV, and per-room market cap) points in the same direction. The business has turned. The market has not noticed yet.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.